ADAS and Autonomous Driving Tier 1 Suppliers Research Report, 2024 - Foreign Companies

Research on foreign ADAS Tier 1 suppliers: make all-round attempts to transform and localize supply chain and teams.???

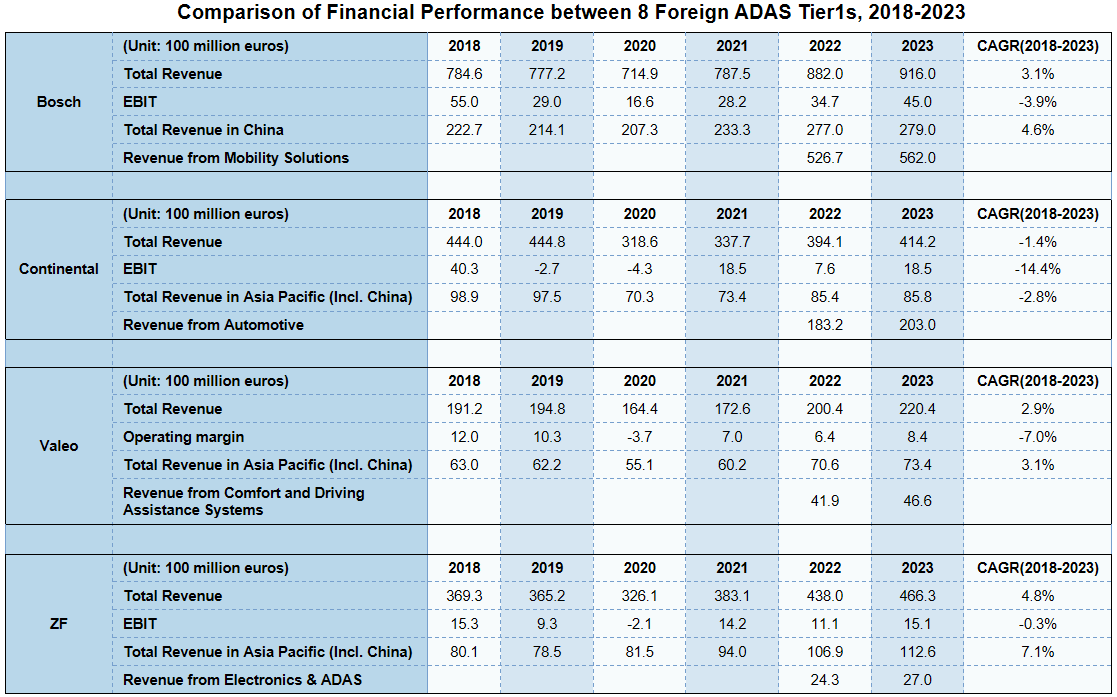

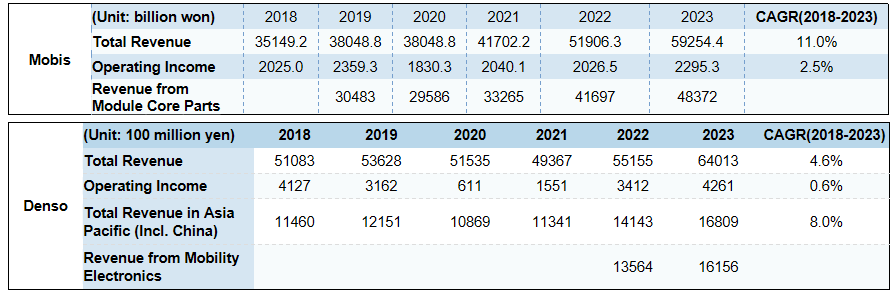

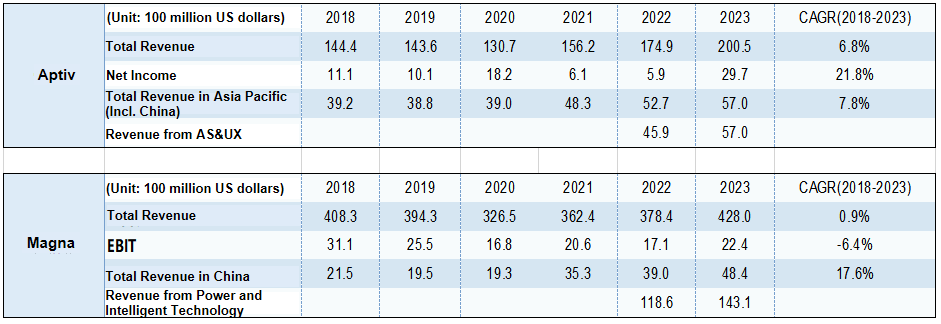

1. Foreign ADAS Tier 1 suppliers fall behind relatively in development of intelligent driving, with declining profitability from 2018 to 2023.

??

In the past few years, foreign ADAS Tier1s like Bosch, Continental, Valeo, ZF and Magna have faced unprecedented challenges. According to the data from 2018 to 2023, the compound annual growth rates (CAGR) of EBIT/operating margin of these five giants were -3.9%, -14.4%, -7%, -0.3% and -6.4%, respectively. These data not only reflect the impact of the global economic environment on traditional auto parts suppliers, but also reveal the intensified competition in vehicle electrification, connectivity, intelligence and sharing.????

2. Reasons why foreign Tier1s lag behind in development of ADAS business.

(1) Difficulty 1 in developing in China: There are many ADAS Tier1 players in white-hot competition.??

As China’s local companies soar in the field of ADAS, foreign Tier 1 suppliers are facing unprecedented pressure of competition. In the past, these foreign giants dominated the Chinese market with their leading technologies and rich experience. Yet as new technologies spring up and China’s local companies rise rapidly, the market pattern is undergoing disruptive changes.?

???

China's local intelligent driving Tier1s have been quickly accepted by the market by virtue of their deep understanding of the local market and great R&D strength. These companies are well-known for their quick response to market needs, cost-effective solutions, and excellent AI algorithm capabilities. Currently there are the following types of players:??

1) Traditional established suppliers like Desay SV and Jingwei Hirain;

2) Algorithm companies that implement "L4 technology generalizing L2++", such as Momenta, WeRide, Pony.ai and Baidu;?

3) Cross-border giants like Huawei: Huawei not only boasts great technical strength, but also has extensive industrial resources and can quickly integrate upstream and downstream resources to provide customers with a full range of intelligent driving solutions;

4) Full-stack self-development OEMs such as NIO and Tesla, which have also shown great innovation capabilities in the field of intelligent driving;

5) Startups including Maxieye, Hong Jing Drive and iMotion, which emerge rapidly, and encroach on the market share of conventional Tier1s through technological innovation and flexible product matrix strategies.??

????

The emergence of these new players has not only broken the competitive edges of traditional Tier 1 suppliers, but also redefined the intelligent vehicle supply chain pattern. As electrification, intelligence and connectivity gather pace, the industry is experiencing a profound transformation. These changes bring structural increment opportunities to the market, while also making the competition among intelligent driving Tier1s in China fiercer.??????

?

(2) Difficulty 2 in developing in China: There is a drastic involution in Chinese L2-L3 market.

In current stage, the competition in the new energy market is stiff. The successful implementation of urban NOA means that OEMs have the technical strength to realize all-scenario driving assistance, which will help them take a lead in the market competition. By rolling out urban NOA on a large scale, major mainstream OEMs have acquired massive and diverse real data and built a forward cycle between data and algorithm solution iterations, thereby creating a technical moat. In addition, as the young generation becomes increasingly important consumers in the automotive market, they have ever higher expectations of intelligence and convenience. As an intelligent function, urban NOA will gradually become one of the key factors to the young generation of consumers making decisions on purchasing a car.??????

In 2023, urban NOA began to show growth spurt. Seen from the new vehicles launched on market, the installation rates of L2 and higher-level ADAS functions rose sharply, of which L2.5 and L2.9 enjoyed a surge. In 2022 the installation rate of L2.5 functions in newly launched passenger cars in China was 13.25%, a figure climbing to 19.86% from January to April 2024; the installation rate of L2.9 functions jumped from 12.4% in 2022 to 23.4%.???

Following Xpeng and Huawei taking the lead in launching urban NOA in Shanghai, Guangzhou and Shenzhen, various automakers have been making intensive efforts in terms of technology path, urban launch scale, implementation speed and cost. The support behind this is mainly from Chinese ADAS Tier1s, and foreign ADAS Tier1s are rarely seen.??

3. Foreign ADAS Tier1s make all-round efforts to transform: from strategic transformation, to redeployment of ADAS/AD product matrix, and then to comprehensive breakthroughs in intelligent driving solutions.??

(1) Step up intelligent driving layout in the Chinese market and strive to achieve the development goal of "in China, for China".??

In Aptiv’s case, it increases its investment in China to deepen its presence in the local market, and plans to operate 70% of its overall business in the Chinese market by 2028. Currently, the company forges closer strategic partnerships with China’s local companies by establishing and expanding R&D centers and building an automotive ecosystem in China, so as to make triple breakthroughs in intelligent driving technology innovation, penetration into the Chinese market, and localization of intelligent driving products.???????

At CES 2024, Aptiv showcased its seventh-generation 4D corner radar developed by a local team in China. The radar is equipped with China’s first integrated radar chip. This not only marks a major technological breakthrough of Aptiv, but also reflects its determination to gain a solid foothold in the Chinese market. Aptiv also launched the first "cockpit-driving-parking" integration solution developed by a Chinese team. Based on a single SoC, the solution integrates cockpit, driving and parking functions.??

?

?

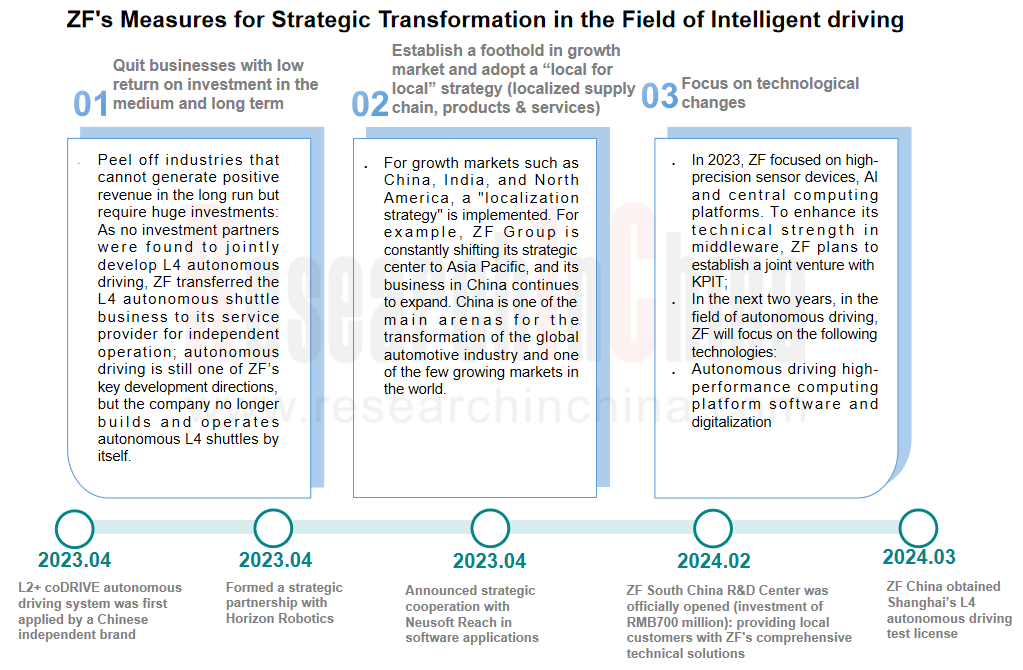

(2) Shift the strategic focus to mass production solutions with higher actual output and commercial value, and peel off high-risk low-return L4 business, to ensure steady business growth.

ZF exhibited a new L4 autonomous shuttle and its previous autonomous shuttle models at CES 2023. Despite being a promising market, autonomous shuttles develop slowly, delaying the expected return on investment. The current economic crisis and the transformation to e-mobility have increased cost pressures, forcing the industry to re-evaluate investment strategies. ZF has decided to reduce high-risk investments, optimize allocation of resources, and focus on projects with clear market demand and a shorter payback period, in a bid to ensure financial health and sustainable development.???

(3) Supply chain localization, team localization, cost-effective intelligent driving solutions + faster cross-domain integration

Foreign Tier1s speed up the launch of more cost-effective intelligent driving solutions for the Chinese market by way of supply chain localization, team localization, strategic cooperation, investment in innovative Chinese intelligent driving companies, and continuous technological innovation. In addition, one of ultimate goals in developing intelligent vehicles is to achieve cross-domain integration, that is, seamlessly integrate various vehicle functions to enable all-around intelligent experiences. The concept of cockpit-driving integration has now entered the substantive implementation stage of quite a few foreign Tier1s, and is evolving towards "integrated chip" solutions.???

?

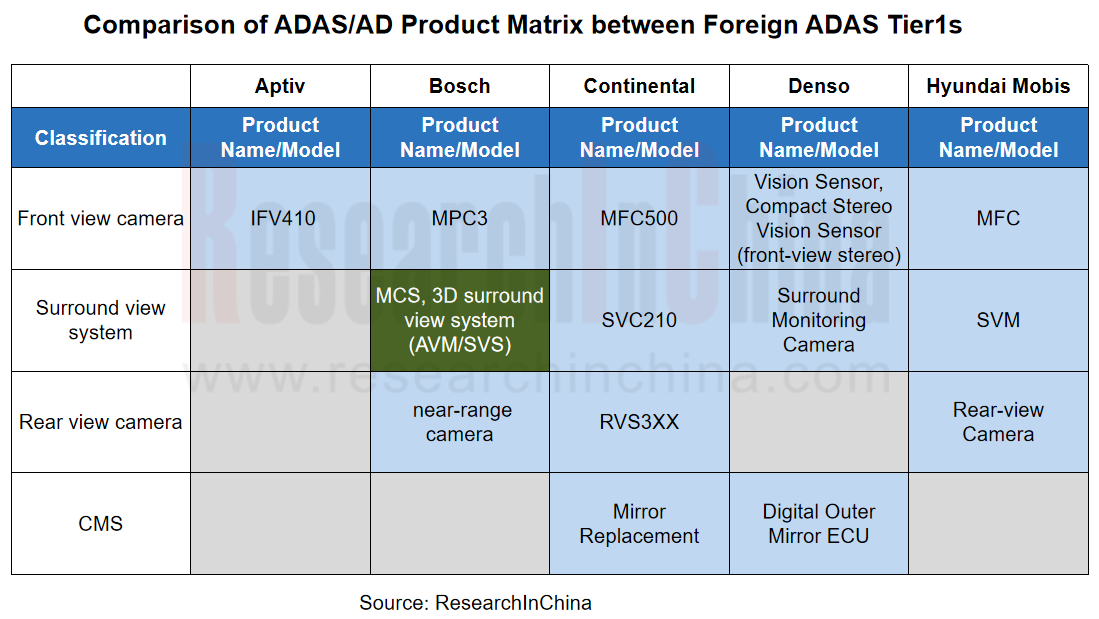

4. A more comprehensive ADAS/AD product matrix allows foreign ADAS Tier1s to stay competitive.?

In terms of product matrix, Bosch, Continental, ZF and Aptiv have the most comprehensive product matrix, and all the eight international Tier 1s have deployed front-view cameras and autonomous driving solutions. In 2023, Bosch abandoned development of LiDAR and put more resources in development of radars. 4D radar and front/rear radar have become the deployment focus of foreign Tier1s during 2023-2024.??

As the core component of central EEA, cross-domain/central computing platforms have been deployed by Aptiv, Bosch, Continental and ZF. Between 2023 and 2024, Aptiv, Bosch, Valeo and Magna accelerate R&D of cockpit-driving cross-domain integration, and presented a demo at CES 2024 or Auto China 2024. Following the new industry trend towards supply chain localization and localized cost-effective products or solutions, Aptiv launched the localized intelligent driving solution of Gen 6 ADAS, and ZF rolled out Pro AI based on Chinese chips.?????

As for high-level intelligent driving solution (NOA), Bosch has successfully achieved mass production and installation in vehicles through its local teams. Continental and Horizon Robotics established Continental Smart Core Technology (Shanghai) Co., Ltd. and launched the Driving-Parking Integration 3.0 solution. They will soon unveil a high-level intelligent driving solution. ZF made a strategic investment in CalmCar, and they jointly rolled out a cost-effective parking solution.???

Note: Blue Boxes refer to the products that have been released; Green Boxes refer to the latest products released between 2023 and 2024; and Gray Boxes refer to products that have not yet been deployed.

1 Global Regulations on Taking Autonomous Driving to Road and Development Plans

1.1 Global Regulations on Taking Autonomous Driving to Road

1.1.1 UN Regulation on Automated Lane Keeping Systems (ALKS) - Main Test Items

1.1.1 UN Regulation on Automated Lane Keeping Systems (ALKS) -System Safety and Fail-Safe Response

1.1.1 UN Regulation on Automated Lane Keeping Systems (ALKS) - Human Machine Interface / Operator Information

1.1.1 UN Regulation on Automated Lane Keeping Systems (ALKS) - Object Detection, Data Storage

1.1.2 Summary of Autonomous Driving Development Plans of Some Countries/Regions

1.2 EU & Europe’s Regulations on Taking Autonomous Driving to Road

1.2.1 German Act on Autonomous Driving

1.2.2 EU & Europe’s Development Plan for Autonomous Driving

1.2.3 EU’s Autonomous Driving Roadmap and 2040 Outlook

1.3 US’ Regulations on Taking Autonomous Driving to Road

1.3.1 US’ Development Plan for Autonomous Driving

1.4 Japan's Regulations on Taking Autonomous Driving to Road

1.4.1 Japan's Action Plan for Realizing Automated Driving 4.0

1.4.2 Japan's Development Plan for Autonomous Driving

1.4.3 Japan's "RoAD to the L4 Project"

1.5 South Korean’s Regulations on Taking Autonomous Driving to Road

1.5.1 South Korean’s Development Plan for Autonomous Driving

2 Development Trends of Products and Solutions of International Tier1s

2.1 Comparison of Financial Performance between Foreign Tier1s, 2018-2023

2.2 Comparison of ADAS/AD Product Matrix (1)

2.2 Comparison of ADAS/AD Product Matrix (2)

2.3 Comparison of Front View Cameras (1)

2.3 Comparison of Front View Cameras (2)

2.4 Comparison of Surround View Systems

2.5 Comparison of OMS

2.6 Comparison of 4D Radars (1)

2.6 Comparison of 4D Radars (2)

2.7 Comparison of CMS

2.8 Comparison of Domain Control/Central Computing Platforms

2.9 Comparison of Autonomous Driving/Driving-Parking Integration Solutions

2.10.1 Difficulties for Foreign Tier1s Developing ADAS Business in China (1)

2.10.2 Difficulties for Foreign Tier1s Developing ADAS Business in China (2)

2.10.3 Difficulties for Foreign Tier1s Developing ADAS Business in China (3)

2.10.4 Difficulties for Foreign Tier1s Developing ADAS Business in China (4)

2.11.1 Advantage of International Tier1s: Background - L3 Gets Ready 2.11.2 Advantage of International Tier1s: L3 Layout

2.11.3 Advantage of International Tier1s: Engineering Solutions

2.12.1 Strategy Trends of International ADAS Tier1s (1)

2.12.2 Strategy Trends of International ADAS Tier1s (2)

2.13.1 Product Trends: 4D Radar Starts Mass Adoption

2.13.2 Product Trends: CMS Is Allowed to Be Installed in Vehicles in China, and Competition in the New Market Is Fierce

2.13.3 Product Trends: Multiple Tier1s Have Launched Cross-Domain/Central Computing Platforms

2.14.1 Solution Trends (1)

2.14.2 Solution Trends (2)

2.14.3 Solution Trends (3)

3 Major Foreign Autonomous Driving Tier1s

3.1 Aptiv

3.1.1 Profile

3.1.2 Operation in 2023

3.1.3 Deployments in Autonomous Driving

3.1.4 Overall Strategic Layout in China (1)

3.1.5 Product Layout in China (1)

3.1.5 Product Layout in China (2)

3.1.5 Product Layout in China (3)

3.1.6 Wind River Software Platform

3.1.7 Product Categories

3.1.8 Autonomous Driving Product Layout

3.1.9 Perception Products - Front View Camera (1)

3.1.9 Perception Products - Front View Camera (2)

3.1.10 Perception Products - 4D Front Radar

3.1.11 Perception Products - Corner Radar (1)

3.1.11 Perception Products - Corner Radar (2)

3.1.12 Decision Products - Domain Controller/Multi-Domain Computing Platform

3.1.13 Solutions – Driving-Parking Integration (1)

3.1.13 Solutions – Driving-Parking Integration (2)

3.1.14 Solutions - Autonomous Driving

3.1.15 Product/Market Planning

3.1.16 Summary

3.2 Bosch

3.2.1 Profile

3.2.2 Operation in 2023

3.2.3 Strategic Layout in China (1)

3.2.3 Strategic Layout in China (2)

3.2.3 Strategic Layout in China (3)

3.2.3 Strategic Layout in China (4)

3.2.3 Strategic Layout in China (5)

3.2.3 Strategic Layout in China (6)

3.2.4 Autonomous Driving Product Matrix (1)

3.2.4 Autonomous Driving Product Matrix (2)

3.2.5 Perception Products - Front View Camera (1)

3.2.5 Perception Products - Front View Camera (2)

3.2.6 Perception Products - Surround View System (1)

3.2.6 Perception Products - Surround View System (2)

3.2.6 Perception Products - Surround View System (3)

3.2.7 Perception Products - 5th Generation Front Radar: Supreme Version

3.2.7 Perception Products - 5th Generation Front Radar: Upgrade Version

3.2.8 Perception Products - 5th Generation Front Radar: Industry Chain

3.2.9 Perception Products - 5th Generation Front Radar: Corner Radar (1)

3.2.9 Perception Products - 5th Generation Front Radar: Corner Radar (2)

3.2.10 Perception Products - LiDAR and 6th Generation Radar

3.2.11 Perception Products - DMS/OMS

3.2.12 Perception Products - Ultrasonic Radar

3.2.13 Decision Products - Domain Controller

3.2.14 Middleware

3.2.15 Solutions - Autonomous Driving

3.2.16 Solutions - Automated Parking (1)

3.2.16 Solutions - Automated Parking (2)

3.2.16 Solutions - Automated Parking (3)

3.2.17 Recent Development Layout/Planning

3.2.18 Autonomous Driving Partners

3.3 Continental

3.3.1 Profile

3.3.2 Operation in 2023

3.3.3 Layout in China (1)

3.3.3 Layout in China (2)

3.3.3 Layout in China (3)

3.3.4 Product Categories

3.3.5 Autonomous Driving Product Layout

3.3.6 Perception Products - Front View Camera (1)

3.3.6 Perception Products - Front View Camera (2)

3.3.7 Perception Products - Rearview Camera (1)

3.3.7 Perception Products - Rearview Camera (2)

3.3.7 Perception Products - Rearview Camera (3)

3.3.8 Perception Products - Surround View System (1)

3.3.8 Perception Products - Surround View System (2)

3.3.9 Perception Products - CMS

3.3.10 Perception Products - DMS (1)

3.3.10 Perception Products - DMS (2)

3.3.10 Perception Products - DMS (3)

3.3.11 Perception Products - OMS (1)

3.3.11 Perception Products - OMS (2)

3.3.12 Perception Products - Front radar (1)

3.3.12 Perception Products - Front radar (2)

3.3.13 Perception Products - Corner Radar

3.3.14 Perception Products - 6th Generation Radar (1)

3.3.14 Perception Products - 6th Generation Radar (2)

3.3.15 Perception Products - LiDAR (1)

3.3.15 Perception Products - LiDAR (2)

3.3.15 Perception Products - LiDAR (3)

3.3.16 Perception Products - Ultrasonic Radar

3.3.17 Decision Products - Domain Controller

3.3.18 Decision Products - Central Computing Platform

3.3.19 Solutions - Autonomous Driving (1)

3.3.19 Solutions - Autonomous Driving (2)

3.3.20 Solutions - Automated Parking

3.3.21 Solutions - Road Data Solution

3.3.22 Autonomous Driving Technologies

3.3.23 Summary

3.4 Denso

3.4.1 Profile

3.4.2 Operation in 2023

3.4.3 Strategic Development Plan for ADAS Business

3.4.4 Product Categories

3.4.5 Autonomous Driving Product Layout (1)

3.4.5 Autonomous Driving Product Layout (2)

3.4.6 New Generation Driving Assistance System - Global Safety Package 3

3.4.7 Perception Products - Front view Camera (1)

3.4.7 Perception Products - Front View Camera (2)

3.4.7 Perception Products - Front View Camera (3)

3.4.8 Perception Products - Surround View System

3.4.9 Perception Products - Front Radar

3.4.10 Perception Products - LiDAR

3.4.11 Perception Products - Ultrasonic Radar

3.4.12 Solutions - ADAS

3.4.13 Solutions - Autonomous Driving

3.4.14 Autonomous Driving Development Roadmap

3.4.15 Deployments in Autonomous Driving

3.5 Hyundai Mobis

3.5.1 Profile

3.5.2 Global Layout

3.5.3 Operation in 2023

3.5.4 Strategic Planning for Next Generation Autonomous Driving Products in 2023

3.5.5 Product Categories

3.5.6 Autonomous Driving Product Layout

3.5.7 Perception Products - Front View Camera

3.5.8 Perception Products - Surround View System

3.5.9 Perception Products - DMS

3.5.10 Perception Products - Radar (1)

3.5.10 Perception Products - Radar (2)

3.5.11 Perception Products - LiDAR & Ultrasonic Radar

3.5.12 Solutions - Autonomous Driving & Automated Parking

3.5.13 Solutions - Automated Parking

3.5.14 Autonomous Concept Car

3.5.15 Autonomous Driving Development Planning

3.5.16 Summary

3.6 Magna

3.6.1 Profile

3.6.2 Operation in 2023

3.6.3 Strategic Planning in Autonomous Driving

3.6.4 Product Categories

3.6.5 Autonomous Driving Product Layout

3.6.6 Perception Products - Front View Camera

3.6.7 Perception Products - Surround View System

3.6.8 Perception Products - CMS

3.6.9 Perception Products - DMS

3.6.10 Perception Products - DMS

3.6.11 Perception Products - 4D Front/Corner Radar

3.6.12 Perception Products - LiDAR & Ultrasonic Radar

3.6.13 Decision Products - Domain Controller & Cross-Domain Platform

3.6.14 Solutions - Autonomous Driving

3.6.15 Solutions - Automated Parking

3.6.16 Autonomous Driving & Intelligent Connection Planning

3.6.17 Summary

3.7 Valeo

3.7.1 Profile

3.7.2 Global Operation in 2023

3.7.3 Strategy Upgrade

3.7.4 Strategic Layout in China

3.7.5 Dynamics in Autonomous Driving, 2023-2024

3.7.6 Autonomous Driving Product Matrix (1)

3.7.6 Autonomous Driving Product Matrix (2)

3.7.7 Perception Products - Front View Camera (1)

3.7.7 Perception Products - Front View Camera (2)

3.7.8 Perception Products - Surround View System (1)

3.7.8 Perception Products - Surround View System (2)

3.7.8 Perception Products - Surround View System (3)

3.7.9 Perception Products - Side View Camera & Ultrasonic Radar

3.7.10 Perception Products - CMS

3.7.11 Perception Products - Radar

3.7.12 Perception Products - LiDAR (1)

3.7.12 Perception Products - LiDAR (2)

3.7.13 ADAS Domain Controller

3.7.14 Solutions - Automated Parking (1)

3.7.14 Solutions - Automated Parking (2)

3.7.14 Solutions - Automated Parking (3)

3.7.14 Solutions - Automated Parking (4)

3.7.14 Solutions - Automated Parking (5)

3.7.14 Solutions - Automated Parking (6)

3.7.15 Solutions - Autonomous Driving

3.7.16 Autonomous Delivery Vehicle - eDeliver4U

3.7.17 Intention Prediction Technology (Move Predict.ai)

3.7.18 360-degree Autonomous Emergency Braking System

3.7.19 Summary

3.8 ZF

3.8.1 Profile

3.8.2 Operation in 2023

3.8.3 Autonomous Driving Strategy (1)

3.8.3 Autonomous Driving Strategy (2)

3.8.3 Autonomous Driving Strategy (3)

3.8.4 Recent Changes in Business Division Structure

3.8.5 Product Categories

3.8.6 Autonomous Driving Product Layout

3.8.7 Perception Products - Front View Camera (1)

3.8.7 Perception Products - Front View Camera (2)

3.8.7 Perception Products - Front View Camera (3)

3.8.8 Perception Products - Surround View System

3.8.9 Perception Products - OMS

3.8.10 Perception Products - 4D Front Radar

3.8.11 Perception Products - Front Radar

3.8.12 Perception Products - LiDAR & Sound Sensor

3.8.13 ProAI Computing Platform (1)

3.8.13 ProAI Computing Platform (2)

3.8.14 Decision Products - Domain Controller & Middleware

3.8.15 Solutions - Autonomous Driving & Driving-Parking Integration

3.8.16 Summary

Autonomous Driving Domain Controller and Central Computing Unit (CCU) Industry Report, 2025

Research on Autonomous Driving Domain Controllers: Monthly Penetration Rate Exceeded 30% for the First Time, and 700T+ Ultrahigh-compute Domain Controller Products Are Rapidly Installed in Vehicles

L...

China Automotive Lighting and Ambient Lighting System Research Report, 2025

Automotive Lighting System Research: In 2025H1, Autonomous Driving System (ADS) Marker Lamps Saw an 11-Fold Year-on-Year Growth and the Installation Rate of Automotive LED Lighting Approached 90...

Ecological Domain and Automotive Hardware Expansion Research Report, 2025

ResearchInChina has released the Ecological Domain and Automotive Hardware Expansion Research Report, 2025, which delves into the application of various automotive extended hardware, supplier ecologic...

Automotive Seating Innovation Technology Trend Research Report, 2025

Automotive Seating Research: With Popularization of Comfort Functions, How to Properly "Stack Functions" for Seating?

This report studies the status quo of seating technologies and functions in aspe...

Research Report on Chinese Suppliers’ Overseas Layout of Intelligent Driving, 2025

Research on Overseas Layout of Intelligent Driving: There Are Multiple Challenges in Overseas Layout, and Light-Asset Cooperation with Foreign Suppliers Emerges as the Optimal Solution at Present

20...

High-Voltage Power Supply in New Energy Vehicle (BMS, BDU, Relay, Integrated Battery Box) Research Report, 2025

The high-voltage power supply system is a core component of new energy vehicles. The battery pack serves as the central energy source, with the capacity of power battery affecting the vehicle's range,...

Automotive Radio Frequency System-on-Chip (RF SoC) and Module Research Report, 2025

Automotive RF SoC Research: The Pace of Introducing "Nerve Endings" such as UWB, NTN Satellite Communication, NearLink, and WIFI into Intelligent Vehicles Quickens

RF SoC (Radio Frequency Syst...

Automotive Power Management ICs and Signal Chain Chips Industry Research Report, 2025

Analog chips are used to process continuous analog signals from the natural world, such as light, sound, electricity/magnetism, position/speed/acceleration, and temperature. They are mainly composed o...

Global and China Electronic Rearview Mirror Industry Report, 2025

Based on the installation location, electronic rearview mirrors can be divided into electronic interior rearview mirrors (i.e., streaming media rearview mirrors) and electronic exterior rearview mirro...

Intelligent Cockpit Tier 1 Supplier Research Report, 2025 (Chinese Companies)

Intelligent Cockpit Tier1 Suppliers Research: Emerging AI Cockpit Products Fuel Layout of Full-Scenario Cockpit Ecosystem

This report mainly analyzes the current layout, innovative products, and deve...

Next-generation Central and Zonal Communication Network Topology and Chip Industry Research Report, 2025

The automotive E/E architecture is evolving towards a "central computing + zonal control" architecture, where the central computing platform is responsible for high-computing-power tasks, and zonal co...

Vehicle-road-cloud Integration and C-V2X Industry Research Report, 2025

Vehicle-side C-V2X Application Scenarios: Transition from R16 to R17, Providing a Communication Base for High-level Autonomous Driving, with the C-V2X On-board Explosion Period Approaching

In 2024, t...

Intelligent Cockpit Patent Analysis Report, 2025

Patent Trend: Three Major Directions of Intelligent Cockpits in 2025

This report explores the development trends of cutting-edge intelligent cockpits from the perspective of patents. The research sco...

Smart Car Information Security (Cybersecurity and Data Security) Research Report, 2025

Research on Automotive Information Security: AI Fusion Intelligent Protection and Ecological Collaboration Ensure Cybersecurity and Data Security

At present, what are the security risks faced by inte...

New Energy Vehicle 800-1000V High-Voltage Architecture and Supply Chain Research Report, 2025

Research on 800-1000V Architecture: to be installed in over 7 million vehicles in 2030, marking the arrival of the era of full-domain high voltage and megawatt supercharging.

In 2025, the 800-1000V h...

Foreign Tier 1 ADAS Suppliers Industry Research Report 2025

Research on Overseas Tier 1 ADAS Suppliers: Three Paths for Foreign Enterprises to Transfer to NOA

Foreign Tier 1 ADAS suppliers are obviously lagging behind in the field of NOA.

In 2024, Aptiv (2.6...

VLA Large Model Applications in Automotive and Robotics Research Report, 2025

ResearchInChina releases "VLA Large Model Applications in Automotive and Robotics Research Report, 2025": The report summarizes and analyzes the technical origin, development stages, application cases...

OEMs’ Next-generation In-vehicle Infotainment (IVI) System Trends Report, 2025

ResearchInChina releases the "OEMs’ Next-generation In-vehicle Infotainment (IVI) System Trends Report, 2025", which sorts out iterative development context of mainstream automakers in terms of infota...