In the automotive sector, MLCC is generally used in power system, safety system, comfort system, entertainment system and so forth. That intelligent driving functions prevail in cars brings strong demand for MLCC. As the intelligentization, networking and electrification of vehicles is galloping, it is expected by industry insiders that MLCC use in cars will soar by folds. In the era of intelligent connected battery electric vehicle (BEV), a single vehicle requires as 6 times MLCCs as that for a current common internal combustion engine.

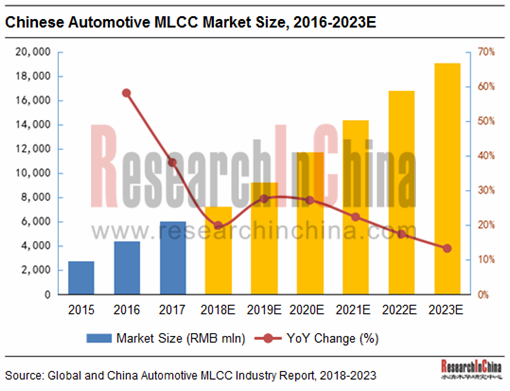

In recent years, electrification of cars is gathering momentum worldwide, and battery electric vehicle (BEV) output keeps soaring year after year, coupled with a steady rise in output of hybrids/PHEVs and smart fuel-efficient models as well as common internal combustion engines going intelligent, all of which serve as a spur to the demand for MLCC. As estimated, the Chinese market size of automotive MLCC will report RMB19.053 billion in 2023 (as compared with RMB6.044 billion in 2017), showing a CAGR of 21.1% between 2017 and 2023.

The well-known automotive MLCC vendors are mainly from Japan, South Korea, Europe & America, and Taiwan (China), of which Japanese companies consist of Murata, TDK, Taiyo Yuden, Kyocera, etc.; South Korean peer refers to Samsung Electro-Mechanics; and Taiwanese counterparts are Yageo and Walsin Technology.

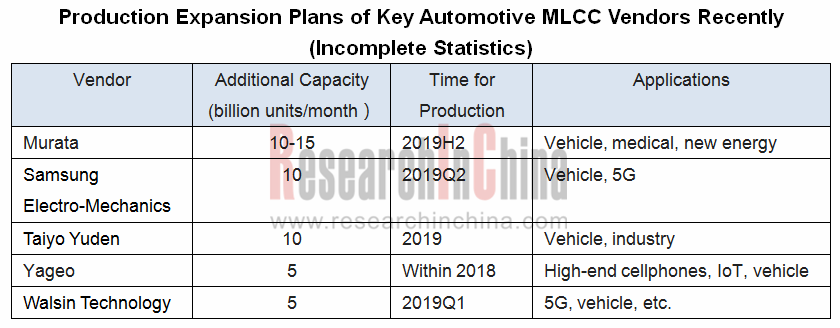

Currently, Murata is the vendor boasting the most market shares worldwide (29%; about 40% in the automotive MLCC market), with the production capacity of 960 billion units/year for the moment. Murata has slashed production of low-end MLCC and related delivery has drawn to an end over the past two years. In 2018, Murata invested $660 million for expanding production of MLCC for medical and automotive use and mass-production is anticipated in 2019.

Samsung Electro-Mechanics has sprung up and has been in the second place worldwide since it outperformed Japan-based TDK in 2009. Impacted by the explosion of Samsung NOTE7, Samsung Electro-Mechanics has tightened control on the quality of products and cut shipments over the recent years, while it planned to invest the additional 10 billion units/month MLCC for cars and 5G products.

TDK canceled product orders involving 700 million MLCCs in 360 models in 2017, and has transferred to focus on medium- and high-end products.

Chinese MLCC vendors has been developing apace over the recent years but are still engaged in supply for consumer electronics. Few companies like Fenghua Advanced Technology have rolled out the products in line with AEC-Q200 criterion. Due to weak strength, Chinese players are still hard to pose a threat to the MLCC giants from Japan, South Korea and Taiwan (China).

The report highlights the following:

MLCC industry overview (definition, classification, policies, etc.);

MLCC industry overview (definition, classification, policies, etc.);

Global and China MLCC markets (market size, production capacity, industrial chains, competitive landscape, etc.);

Global and China automotive MLCC markets (market size, production capacity, competitive pattern, etc.);

Eleven automotive MLCC vendors including Murata, Samsung Electro-Mechanics, Kyocera, Taiyo Yuden, TDK, KEMET, Fenghua Advanced Technology, Walsin Technology, Yageo, HolyStone and Chemi-Con (profile, financials, hit products, R&D, manufacturing bases, technical features, etc.);

Eight manufacturers in the upstream of MLCC, including Sakai Chemical Industry, Ferro, Prosperities Dielectrics, Shandong Sinocera Functional Material, Nippon Chemical Industrial, SHOEI, Sumitomo Metal Industries, and ESL.

China Automotive Lighting and Ambient Lighting System Research Report, 2025

Automotive Lighting System Research: In 2025H1, Autonomous Driving System (ADS) Marker Lamps Saw an 11-Fold Year-on-Year Growth and the Installation Rate of Automotive LED Lighting Approached 90...

Ecological Domain and Automotive Hardware Expansion Research Report, 2025

ResearchInChina has released the Ecological Domain and Automotive Hardware Expansion Research Report, 2025, which delves into the application of various automotive extended hardware, supplier ecologic...

Automotive Seating Innovation Technology Trend Research Report, 2025

Automotive Seating Research: With Popularization of Comfort Functions, How to Properly "Stack Functions" for Seating?

This report studies the status quo of seating technologies and functions in aspe...

Research Report on Chinese Suppliers’ Overseas Layout of Intelligent Driving, 2025

Research on Overseas Layout of Intelligent Driving: There Are Multiple Challenges in Overseas Layout, and Light-Asset Cooperation with Foreign Suppliers Emerges as the Optimal Solution at Present

20...

High-Voltage Power Supply in New Energy Vehicle (BMS, BDU, Relay, Integrated Battery Box) Research Report, 2025

The high-voltage power supply system is a core component of new energy vehicles. The battery pack serves as the central energy source, with the capacity of power battery affecting the vehicle's range,...

Automotive Radio Frequency System-on-Chip (RF SoC) and Module Research Report, 2025

Automotive RF SoC Research: The Pace of Introducing "Nerve Endings" such as UWB, NTN Satellite Communication, NearLink, and WIFI into Intelligent Vehicles Quickens

RF SoC (Radio Frequency Syst...

Automotive Power Management ICs and Signal Chain Chips Industry Research Report, 2025

Analog chips are used to process continuous analog signals from the natural world, such as light, sound, electricity/magnetism, position/speed/acceleration, and temperature. They are mainly composed o...

Global and China Electronic Rearview Mirror Industry Report, 2025

Based on the installation location, electronic rearview mirrors can be divided into electronic interior rearview mirrors (i.e., streaming media rearview mirrors) and electronic exterior rearview mirro...

Intelligent Cockpit Tier 1 Supplier Research Report, 2025 (Chinese Companies)

Intelligent Cockpit Tier1 Suppliers Research: Emerging AI Cockpit Products Fuel Layout of Full-Scenario Cockpit Ecosystem

This report mainly analyzes the current layout, innovative products, and deve...

Next-generation Central and Zonal Communication Network Topology and Chip Industry Research Report, 2025

The automotive E/E architecture is evolving towards a "central computing + zonal control" architecture, where the central computing platform is responsible for high-computing-power tasks, and zonal co...

Vehicle-road-cloud Integration and C-V2X Industry Research Report, 2025

Vehicle-side C-V2X Application Scenarios: Transition from R16 to R17, Providing a Communication Base for High-level Autonomous Driving, with the C-V2X On-board Explosion Period Approaching

In 2024, t...

Intelligent Cockpit Patent Analysis Report, 2025

Patent Trend: Three Major Directions of Intelligent Cockpits in 2025

This report explores the development trends of cutting-edge intelligent cockpits from the perspective of patents. The research sco...

Smart Car Information Security (Cybersecurity and Data Security) Research Report, 2025

Research on Automotive Information Security: AI Fusion Intelligent Protection and Ecological Collaboration Ensure Cybersecurity and Data Security

At present, what are the security risks faced by inte...

New Energy Vehicle 800-1000V High-Voltage Architecture and Supply Chain Research Report, 2025

Research on 800-1000V Architecture: to be installed in over 7 million vehicles in 2030, marking the arrival of the era of full-domain high voltage and megawatt supercharging.

In 2025, the 800-1000V h...

Foreign Tier 1 ADAS Suppliers Industry Research Report 2025

Research on Overseas Tier 1 ADAS Suppliers: Three Paths for Foreign Enterprises to Transfer to NOA

Foreign Tier 1 ADAS suppliers are obviously lagging behind in the field of NOA.

In 2024, Aptiv (2.6...

VLA Large Model Applications in Automotive and Robotics Research Report, 2025

ResearchInChina releases "VLA Large Model Applications in Automotive and Robotics Research Report, 2025": The report summarizes and analyzes the technical origin, development stages, application cases...

OEMs’ Next-generation In-vehicle Infotainment (IVI) System Trends Report, 2025

ResearchInChina releases the "OEMs’ Next-generation In-vehicle Infotainment (IVI) System Trends Report, 2025", which sorts out iterative development context of mainstream automakers in terms of infota...

Autonomous Driving SoC Research Report, 2025

High-level intelligent driving penetration continues to increase, with large-scale upgrading of intelligent driving SoC in 2025

In 2024, the total sales volume of domestic passenger cars in China was...