Autonomous heavy truck research: front runners first going public

Our Autonomous Heavy Truck Industry Report, 2020-2021 carries out research into highway scenario-oriented autonomous heavy truck industry, including OEMs and autonomous driving solution providers inside and outside China.

Several autonomous heavy truck companies try to list their shares for financing.

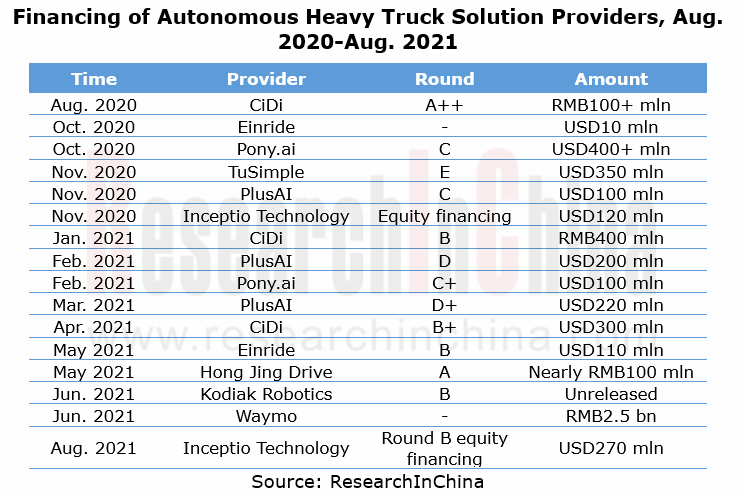

The surging road freight volume and a widening gap in demand for truck drivers, promote the financing boom of self-driving heavy truck industry, and accelerate the R&D of related products and technology landing.

According to incomplete statistics, several autonomous heavy truck solution providers at home and abroad have closed a total of at least 16 funding rounds in the most recent year (August 2020 to August 2021). Examples include PlusAI and Inceptio Technology, two Chinese firms which have raised over USD800 million in all in their recent several funding rounds.

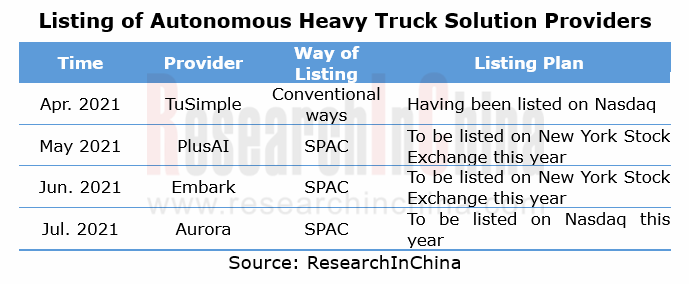

In the meanwhile, some solution providers which suffered sustained losses, and high input and low output, have started resorting to IPO for raising more funds. On April 15, 2021, TuSimple went public on Nasdaq, becoming the world’s first listed company in autonomous driving field. And then a few other autonomous heavy truck solution providers announced listing in the US as special purpose acquisition companies (SPAC).

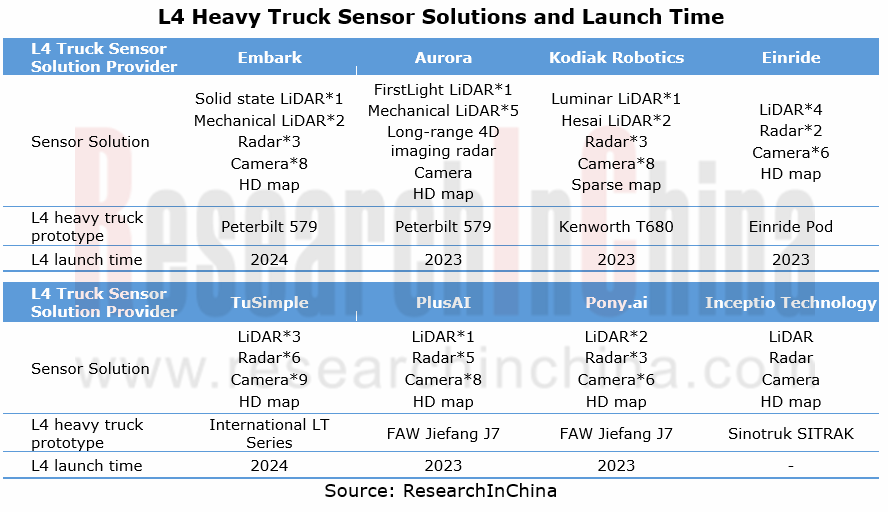

The LiDAR + camera + radar fusion solutions have become mainstream.

Most providers adopt the LiDAR + camera + radar fusion solutions combined with HD map and high-precision positioning, which enable their heavy trucks to drive themselves. Some solution providers like Embark use hybrid LiDAR solutions, that is, the combination of solid-state and mechanical LiDARs enables omnidirectional depth perception of the surroundings of a vehicle.

The time that mainstream solution providers inside and outside China are expected to launch the technology is relatively consistent. In the case of loose policies, autonomous heavy trucks will come into service on highways between 2023 and 2024.

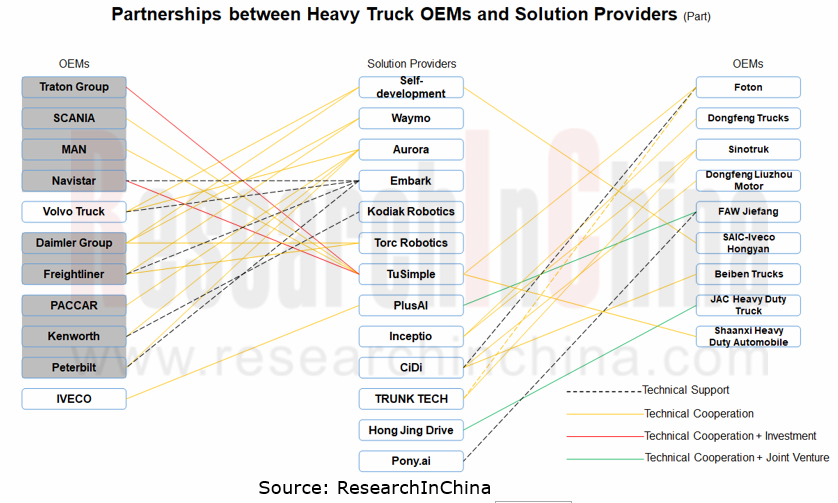

Cooperation modes of autonomous heavy truck industry

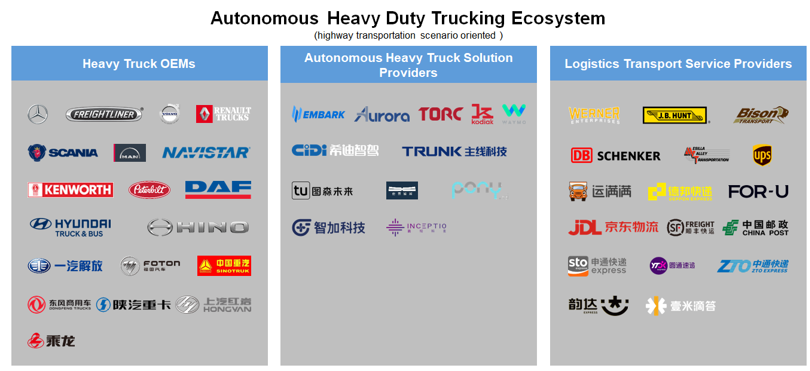

Quite a few heavy truck OEMs and logistics companies race to land on highway scenarios in addition to capital betting on autonomous heavy trucks.

The highway transportation scenario-oriented autonomous heavy truck ecosystem accommodates autonomous heavy truck solution providers, heavy truck manufacturers and logistics transport service providers, which work together to propel commercialization of autonomous heavy trucks. As concerns research and development, solution providers and heavy truck manufacturers jointly develop L4 autonomous heavy trucks based on OEM or AM vehicle models. With regard to commercial operation, solution providers partner with logistics transport service providers on commercial operation and actual freight transport test of autonomous heavy trucks.

In terms of partnerships, autonomous heavy truck solution providers often team up with OEMs, co-developing L4 autonomous heavy trucks based on flagship models in OEM or AM market. Foreign autonomous heavy truck companies develop autonomous driving often under the leadership of their group companies, which means sub-brands of these group companies build technological cooperation with solution providers. For example, Traton under Volkswagen formed a global partnership with TuSimple to jointly develop L4 autonomous driving technology and apply to Volkswagen’s brands like SCANIA and MAN.

Development trends of autonomous heavy trucks

Trend 1: to achieve the goal of “emissions peak in 2030, carbon neutrality in 2060”, the power source of autonomous heavy trucks will shift from diesel to low or zero carbon energy like natural gas and hydrogen.

Trend 2: platooning technology is being reviewed. In January 2019, Daimler Trucks held a contrary opinion on platooning. After thousands of miles of testing, Daimler has come to the conclusion that truck platooning delivers low economic benefits and has natural defects such as needing a driver, so it will end development of the technology and turn to L4 autonomous heavy trucks. Also, what impacts the actual use of platooning will put on the normal traffic has yet to be verified in real road tests.

In the short run, there will be certain barriers to large-scale commercial use of autonomous heavy trucks in China’s business environment.

The development goal of L4 autonomous heavy trucks is to remove driver and let vehicles complete logistics transport and delivery without needing a human driver to monitor. The most direct customers are logistics companies which operate their own fleets, such as JD, SF Express, YTO Express, STO Express, ZTO Express and YunDa Express. Such companies have much expectation of autonomous heavy trucks lowering their total cost of ownership (TCO), which will make autonomous heavy trucks a big market.

In China, truck drivers are generally self-employed and only 17% of them have their vehicles employed by companies or owned by fleets; 83% drive their own vehicles, according to the Survey Report on Employment of Truck Drivers in 2021 released by China Federation of Logistics & Purchasing (CFLP). The blossom of autonomous heavy trucks in China is still a long way off.

China Automotive Lighting and Ambient Lighting System Research Report, 2025

Automotive Lighting System Research: In 2025H1, Autonomous Driving System (ADS) Marker Lamps Saw an 11-Fold Year-on-Year Growth and the Installation Rate of Automotive LED Lighting Approached 90...

Ecological Domain and Automotive Hardware Expansion Research Report, 2025

ResearchInChina has released the Ecological Domain and Automotive Hardware Expansion Research Report, 2025, which delves into the application of various automotive extended hardware, supplier ecologic...

Automotive Seating Innovation Technology Trend Research Report, 2025

Automotive Seating Research: With Popularization of Comfort Functions, How to Properly "Stack Functions" for Seating?

This report studies the status quo of seating technologies and functions in aspe...

Research Report on Chinese Suppliers’ Overseas Layout of Intelligent Driving, 2025

Research on Overseas Layout of Intelligent Driving: There Are Multiple Challenges in Overseas Layout, and Light-Asset Cooperation with Foreign Suppliers Emerges as the Optimal Solution at Present

20...

High-Voltage Power Supply in New Energy Vehicle (BMS, BDU, Relay, Integrated Battery Box) Research Report, 2025

The high-voltage power supply system is a core component of new energy vehicles. The battery pack serves as the central energy source, with the capacity of power battery affecting the vehicle's range,...

Automotive Radio Frequency System-on-Chip (RF SoC) and Module Research Report, 2025

Automotive RF SoC Research: The Pace of Introducing "Nerve Endings" such as UWB, NTN Satellite Communication, NearLink, and WIFI into Intelligent Vehicles Quickens

RF SoC (Radio Frequency Syst...

Automotive Power Management ICs and Signal Chain Chips Industry Research Report, 2025

Analog chips are used to process continuous analog signals from the natural world, such as light, sound, electricity/magnetism, position/speed/acceleration, and temperature. They are mainly composed o...

Global and China Electronic Rearview Mirror Industry Report, 2025

Based on the installation location, electronic rearview mirrors can be divided into electronic interior rearview mirrors (i.e., streaming media rearview mirrors) and electronic exterior rearview mirro...

Intelligent Cockpit Tier 1 Supplier Research Report, 2025 (Chinese Companies)

Intelligent Cockpit Tier1 Suppliers Research: Emerging AI Cockpit Products Fuel Layout of Full-Scenario Cockpit Ecosystem

This report mainly analyzes the current layout, innovative products, and deve...

Next-generation Central and Zonal Communication Network Topology and Chip Industry Research Report, 2025

The automotive E/E architecture is evolving towards a "central computing + zonal control" architecture, where the central computing platform is responsible for high-computing-power tasks, and zonal co...

Vehicle-road-cloud Integration and C-V2X Industry Research Report, 2025

Vehicle-side C-V2X Application Scenarios: Transition from R16 to R17, Providing a Communication Base for High-level Autonomous Driving, with the C-V2X On-board Explosion Period Approaching

In 2024, t...

Intelligent Cockpit Patent Analysis Report, 2025

Patent Trend: Three Major Directions of Intelligent Cockpits in 2025

This report explores the development trends of cutting-edge intelligent cockpits from the perspective of patents. The research sco...

Smart Car Information Security (Cybersecurity and Data Security) Research Report, 2025

Research on Automotive Information Security: AI Fusion Intelligent Protection and Ecological Collaboration Ensure Cybersecurity and Data Security

At present, what are the security risks faced by inte...

New Energy Vehicle 800-1000V High-Voltage Architecture and Supply Chain Research Report, 2025

Research on 800-1000V Architecture: to be installed in over 7 million vehicles in 2030, marking the arrival of the era of full-domain high voltage and megawatt supercharging.

In 2025, the 800-1000V h...

Foreign Tier 1 ADAS Suppliers Industry Research Report 2025

Research on Overseas Tier 1 ADAS Suppliers: Three Paths for Foreign Enterprises to Transfer to NOA

Foreign Tier 1 ADAS suppliers are obviously lagging behind in the field of NOA.

In 2024, Aptiv (2.6...

VLA Large Model Applications in Automotive and Robotics Research Report, 2025

ResearchInChina releases "VLA Large Model Applications in Automotive and Robotics Research Report, 2025": The report summarizes and analyzes the technical origin, development stages, application cases...

OEMs’ Next-generation In-vehicle Infotainment (IVI) System Trends Report, 2025

ResearchInChina releases the "OEMs’ Next-generation In-vehicle Infotainment (IVI) System Trends Report, 2025", which sorts out iterative development context of mainstream automakers in terms of infota...

Autonomous Driving SoC Research Report, 2025

High-level intelligent driving penetration continues to increase, with large-scale upgrading of intelligent driving SoC in 2025

In 2024, the total sales volume of domestic passenger cars in China was...