Research on autonomous delivery: the cost declines, and the pace of penetration and deployment in scenarios accelerate.

Autonomous delivery contains outdoor autonomous delivery (including ground-based delivery and drone delivery) and indoor robot delivery. This report focuses on researching outdoor ground-based autonomous delivery vehicles.

1. The autonomous delivery industry has transitioned from test run to large-scale operation.

In May 2021, the first batch of autonomous delivery vehicles in China was allowed to run on public roads in demonstration areas. During the epidemic in Shanghai in 2022, more than 500 autonomous delivery vehicles were assembled to serve the affected areas. After going through adaptation to different scenarios and technical optimization and verification in this period of time, autonomous delivery vehicles are finding ever wider application. Autonomous express delivery, autonomous takeaway delivery, supermarket delivery and autonomous retail have penetrated scenarios like communities, industrial parks, college campuses, smart scenic spots, AI parks and business districts.

In Neolix’s case, as of July 2022 its autonomous vehicles have successfully been used in over 100 scenarios in 40 cities of 13 countries, delivering more than 2 million orders to over 300,000 users. The company has delivered and deployed a total of more than 1,000 vehicles. In the meantime, Unity Drive’s products have landed in over 100 large- and medium-sized cities and run in over 150 parks across China. As of July 2022, GoFurther.AI’s intelligent autonomous delivery vehicles have delivered 1.3 million parcels.

As concerns application, as of May 2022, JD Logistics has had nearly 400 intelligent delivery vehicles operated normally in over 25 cities across China, including Beijing, Tianjin and Changshu. During 2022-2023, JD will push on with research and development and put into use thousands of intelligent delivery vehicles for a wider coverage of autonomous delivery. In more than 200 colleges and universities in China, Cainiao has introduced more than 500 Xiaomanlu autonomous vehicles to serve millions of teachers and students, realizing normal operation.

Companies’ quicker pace of carrying out their large-scale implementation plans has a strong bond with maturing autonomous delivery vehicle technology and declining vehicle cost.

2. The partnerships between industry chain companies expand, and the cost of autonomous delivery vehicles dwindles.

In April 2022, Haomo.AI introduced Little Magic Camel, an intelligent vehicle packing 3 mechanical LiDARs and a 360TOPS computing platform. The price of the vehicle is as low as RMB130,000, equivalent to the annual salary of a courier working in a big city.

Previously, the prices of autonomous delivery vehicles ranged at RMB500,000-600,000 in 2020, and dropped to RMB200,000-300,000 in 2021 before falling to RMB130,000 in 2022. From 2023 to 2025, the cost of autonomous delivery vehicles will be lowered to less than RMB100,000.

Autonomous delivery vehicles vary in specification and functional purpose, and their prices thus differ greatly as a matter of course. In addition to prices, autonomous vehicles also come with hidden costs. Almost all ongoing autonomous delivery projects are equipped with autonomous driving engineers to participate in the whole process or remotely control at the backend, in a bid to intervene at any time in the case of emergencies.

Unity Drive’s remote cockpit (ultralow latency: ≤50ms)

From a cost perspective, autonomous delivery vehicles have yet to gain a big replacement edge over labor. The adoption of autonomous delivery vehicles at the earliest and acquisition of more long-tail scenario data is the only path for products and technology to mature.

The autonomous delivery vehicle market has boosted development of local components suppliers. Independent components companies participate in the autonomous delivery supply chain more deeply, and autonomous delivery vehicle manufacturers also cut down their costs with the help of local suppliers. Taking LiDAR as an example, Modai 20 carries Hesai long-range high-resolution Pandar Series LiDAR and mid-range XT Series LiDAR; GoFurther.AI’s autonomous delivery vehicles bear the combined LiDAR solution (RS-LiDAR-16+RS-Bpearl) from RoboSense.

As companies promote and deploy their projects on large scale, especially signing city-level contracts (e.g., Unity Drive + Yancheng City, MOVE-X + Wuwei City, and JD + Changshu City), the hardware and O&M costs per autonomous delivery vehicle will be reduced with bulk purchase.

At present, both production capacity and output of autonomous delivery vehicles in China keeps growing. For example, MOVE-X’s smart factory boasts planned annual capacity of 20,000 units; Haomo.AI already has annual capacity of 10,000 units.

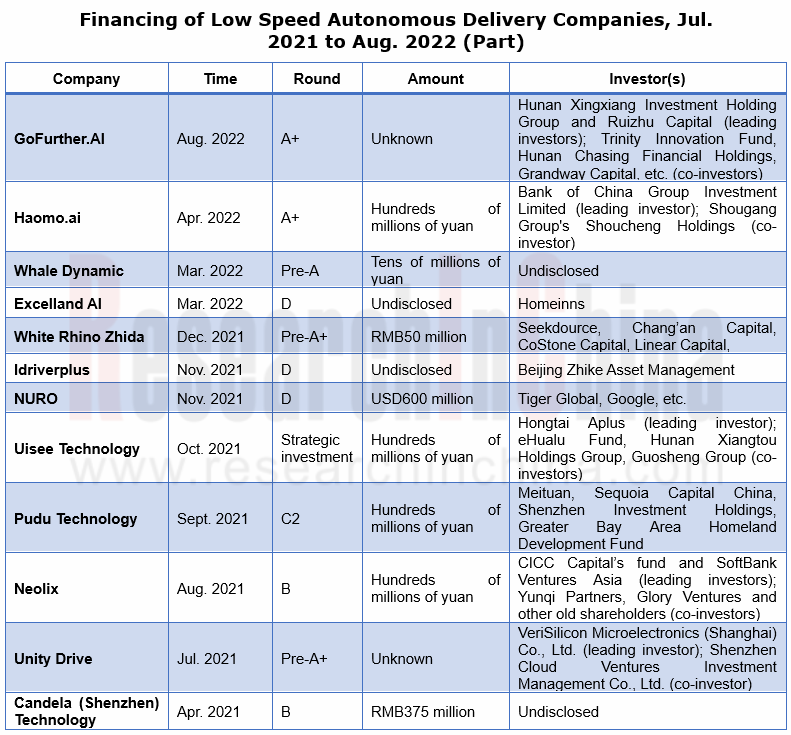

The development of autonomous delivery vehicles is inseparable from capital support. In the past year, autonomous delivery companies like Pudu Technology and Neolix acquired hundreds of millions of yuan in investment.

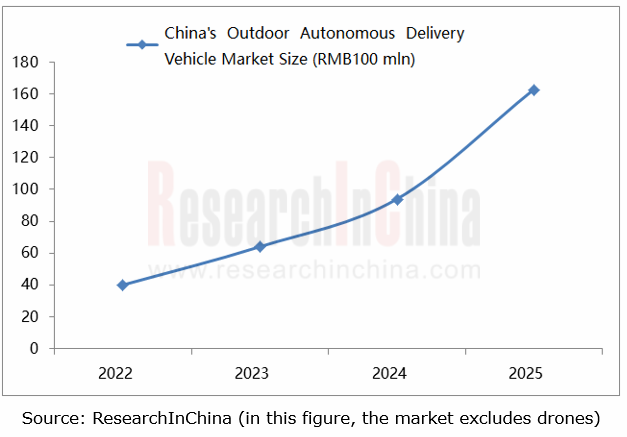

3. The autonomous delivery market sustains rapid growth and will be worth RMB17 billion in 2025.

According to data from State Post Bureau of China, from January to July 2022, the courier service companies in China handled a total of 60.87 billion parcels (including 51.22 billion pieces delivered from January to June, a year-on-year increase of 3.7%, and 9.65 billion pieces in July, up 8.0%). By the end of 2021, express couriers in China have numbered 4.5 million, and food takeout delivery riders have exceeded 13 million, including 6 million Meituan riders.

Companies badly need to reduce costs and improve efficiency. Meituan plans to deploy 10,000 autonomous delivery vehicles nationwide within three years. On our estimate, China's outdoor autonomous delivery vehicle market will be valued at about RMB17 billion in 2025.

Some companies are also exploring new models for how to maximize efficiency of cooperative delivery between manpower and machines. For example, the autonomous delivery vehicle adoption program launched by JD is a typical case.

To reduce work intensity of couriers, JD Logistics has introduced "Autonomous Vehicle Adoption Program". In areas covered by autonomous delivery, the couriers of JD Logistics can apply for "adoption" of a certain number of autonomous delivery vehicles to help them work. Couriers thus become the "commander" of a robot delivery squad, handing the standard delivery work over to autonomous delivery vehicles, and themselves take on dynamic collection or other personalized services. This adoption program has favored an over 50% growth in JD’s order delivery during peak seasons.

4. Autonomous delivery vehicles have a greater ability to connect scenarios.

Connecting to more public roads:

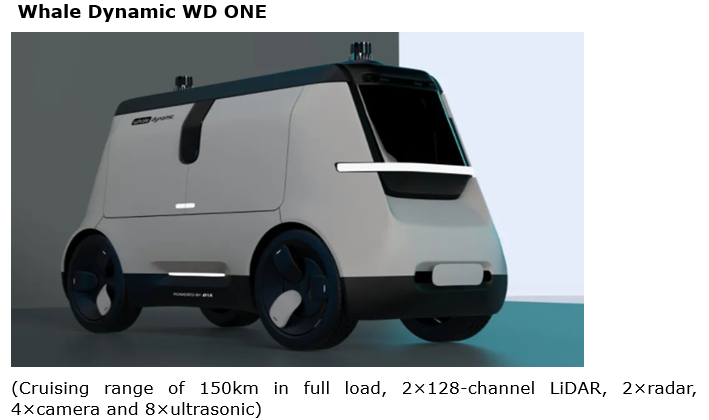

From fixed-area scenarios (e.g., campuses, scenic spots, communities, demonstration areas, hospitals and factories) to densely populated business districts, plazas and subway entrances, autonomous delivery is becoming more widespread, and plus continuous technological iterations and Corner Case scenario data accumulation, autonomous delivery vehicles offer higher safety and reliability and are applicable to more public road scenarios. Some companies have begun to enhance their road-level autonomous delivery business. One example is Whale Dynamic.

Whale Dynamic uses L4 passenger car autonomous driving technology to build integrated solutions for small autonomous vehicles, targeting the road autonomous delivery market.

In September 2021, Alibaba announced that DAMO Academy is working to develop "Damanlu", a L4 autonomous light truck product for urban distribution scenarios, delivering goods from distribution stations to Cainiao Courier Stations in parks. In June 2022, Deqing County of Zhejiang became China’s first city to issue public road test licenses for L4 autonomous trucks with “no people at the driver’s seat”, and Alibaba acquired one of the first two licenses. Damanlu carried out road tests in designated areas in Deqing, including some highway sections.

There are also companies trying to get through terminal distribution within 5 kilometers outdoors and enable free mobility in indoor and semi-enclosed environments. For example, Candela's split product, the Sunny new-generation autonomous logistics vehicle features automatic unloading and loading cabinet, real-time obstacle avoidance, cloud mapping, and multi-vehicle intelligent scheduling. The front large screen has the capabilities of human-computer interaction and advertising display. The vehicle has come into commercial operation. Candela realizes the seamless connection of indoor and outdoor logistics and distribution through the cooperative scheduling of outdoor Sunny autonomous vehicles and indoor Candlelight robots.

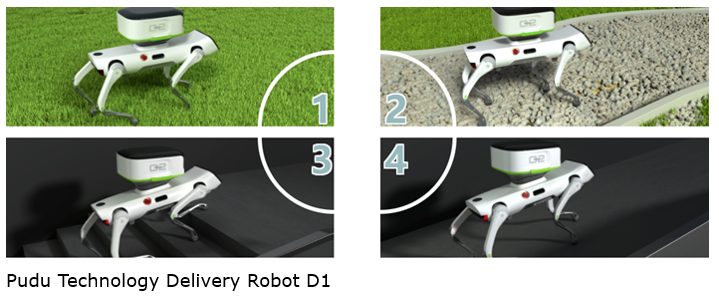

Unlike wheeled autonomous vehicles, quadruped robots are among the most complex and challenging types in robotics industry. On March 24, 2022, Pudu Technology unveiled D1, a quadruped delivery robot equipped with a dedicated pan-tilt delivery box. The active control via control algorithm allows pan-tilt delivery box to automatically adjust pitch attitude. When the robot walks and climbs slopes, the pan-tilt delivery box can always stay level. D1 can be used for the "last-three-kilometer" delivery in office buildings, parks, and residential quarters.

In January 2022, R3, the third-generation battery electric autonomous delivery vehicle jointly developed and designed by BYD and Nuro, made a debut. The biggest feature of this vehicle is the airbag installed outside to protect pedestrians on roads. The model is expected to be mass-produced in 2023.

At present, the logistics and food delivery giants, JD, Meituan and Cainiao are each phasing in their plans of introducing 10,000 autonomous delivery vehicles in the next three years. Other players have also increased the activities of daily autonomous delivery. White Rhino Zhida plans to realize daily delivery by 5,000 autonomous vehicles within five years.

China Automotive Lighting and Ambient Lighting System Research Report, 2025

Automotive Lighting System Research: In 2025H1, Autonomous Driving System (ADS) Marker Lamps Saw an 11-Fold Year-on-Year Growth and the Installation Rate of Automotive LED Lighting Approached 90...

Ecological Domain and Automotive Hardware Expansion Research Report, 2025

ResearchInChina has released the Ecological Domain and Automotive Hardware Expansion Research Report, 2025, which delves into the application of various automotive extended hardware, supplier ecologic...

Automotive Seating Innovation Technology Trend Research Report, 2025

Automotive Seating Research: With Popularization of Comfort Functions, How to Properly "Stack Functions" for Seating?

This report studies the status quo of seating technologies and functions in aspe...

Research Report on Chinese Suppliers’ Overseas Layout of Intelligent Driving, 2025

Research on Overseas Layout of Intelligent Driving: There Are Multiple Challenges in Overseas Layout, and Light-Asset Cooperation with Foreign Suppliers Emerges as the Optimal Solution at Present

20...

High-Voltage Power Supply in New Energy Vehicle (BMS, BDU, Relay, Integrated Battery Box) Research Report, 2025

The high-voltage power supply system is a core component of new energy vehicles. The battery pack serves as the central energy source, with the capacity of power battery affecting the vehicle's range,...

Automotive Radio Frequency System-on-Chip (RF SoC) and Module Research Report, 2025

Automotive RF SoC Research: The Pace of Introducing "Nerve Endings" such as UWB, NTN Satellite Communication, NearLink, and WIFI into Intelligent Vehicles Quickens

RF SoC (Radio Frequency Syst...

Automotive Power Management ICs and Signal Chain Chips Industry Research Report, 2025

Analog chips are used to process continuous analog signals from the natural world, such as light, sound, electricity/magnetism, position/speed/acceleration, and temperature. They are mainly composed o...

Global and China Electronic Rearview Mirror Industry Report, 2025

Based on the installation location, electronic rearview mirrors can be divided into electronic interior rearview mirrors (i.e., streaming media rearview mirrors) and electronic exterior rearview mirro...

Intelligent Cockpit Tier 1 Supplier Research Report, 2025 (Chinese Companies)

Intelligent Cockpit Tier1 Suppliers Research: Emerging AI Cockpit Products Fuel Layout of Full-Scenario Cockpit Ecosystem

This report mainly analyzes the current layout, innovative products, and deve...

Next-generation Central and Zonal Communication Network Topology and Chip Industry Research Report, 2025

The automotive E/E architecture is evolving towards a "central computing + zonal control" architecture, where the central computing platform is responsible for high-computing-power tasks, and zonal co...

Vehicle-road-cloud Integration and C-V2X Industry Research Report, 2025

Vehicle-side C-V2X Application Scenarios: Transition from R16 to R17, Providing a Communication Base for High-level Autonomous Driving, with the C-V2X On-board Explosion Period Approaching

In 2024, t...

Intelligent Cockpit Patent Analysis Report, 2025

Patent Trend: Three Major Directions of Intelligent Cockpits in 2025

This report explores the development trends of cutting-edge intelligent cockpits from the perspective of patents. The research sco...

Smart Car Information Security (Cybersecurity and Data Security) Research Report, 2025

Research on Automotive Information Security: AI Fusion Intelligent Protection and Ecological Collaboration Ensure Cybersecurity and Data Security

At present, what are the security risks faced by inte...

New Energy Vehicle 800-1000V High-Voltage Architecture and Supply Chain Research Report, 2025

Research on 800-1000V Architecture: to be installed in over 7 million vehicles in 2030, marking the arrival of the era of full-domain high voltage and megawatt supercharging.

In 2025, the 800-1000V h...

Foreign Tier 1 ADAS Suppliers Industry Research Report 2025

Research on Overseas Tier 1 ADAS Suppliers: Three Paths for Foreign Enterprises to Transfer to NOA

Foreign Tier 1 ADAS suppliers are obviously lagging behind in the field of NOA.

In 2024, Aptiv (2.6...

VLA Large Model Applications in Automotive and Robotics Research Report, 2025

ResearchInChina releases "VLA Large Model Applications in Automotive and Robotics Research Report, 2025": The report summarizes and analyzes the technical origin, development stages, application cases...

OEMs’ Next-generation In-vehicle Infotainment (IVI) System Trends Report, 2025

ResearchInChina releases the "OEMs’ Next-generation In-vehicle Infotainment (IVI) System Trends Report, 2025", which sorts out iterative development context of mainstream automakers in terms of infota...

Autonomous Driving SoC Research Report, 2025

High-level intelligent driving penetration continues to increase, with large-scale upgrading of intelligent driving SoC in 2025

In 2024, the total sales volume of domestic passenger cars in China was...