China Automotive Distribution and Aftermarket Industry Report, 2020-2026

Since 4S store model was introduced in China at the end of the 20th century, China’s authorized dealer system has made a shift from single stores to corporate operation and from extensive management to fine management. For the upstream raw materials, components suppliers provide an array of components to automakers; at the midstream end are automakers which take on design, R&D, manufacture and branding; dealers are downstream players responsible for selling new vehicles and offering aftermarket services. In the whole industry chain, automakers that manage dealers by authorization and rebate policy play a dominant role and have a big say.

In 2019, China produced 25.72 million automobiles and sold 25.77 million units, down 7.5% and 8.2% on the previous year, up 3.3 and 5.4 percentage points, separately, according to the China Association of Automobile Manufacturers (CAAM). China’s automobile circulation industry faces unprecedented challenges as the automobile market is getting through an ever-colder winter. The automotive distribution industry however performs well as a whole. The data from the China Automobile Dealers Association (CADA) shows that in 2019, the top 100 dealers reported a combined output value of RMB1.74 trillion, up 6.3% compared with RMB1.63 trillion in 2018; their total asset investment was RMB802.4 billion, 5.7% less than in 2018 (RMB851.1 billion). In 2019, there were a total of 6,038 4S outlets in China, down 7.5% versus 2018 (6,529); total employment was 420,000 persons, a reduction of 10.6% from 470,000 in 2018.

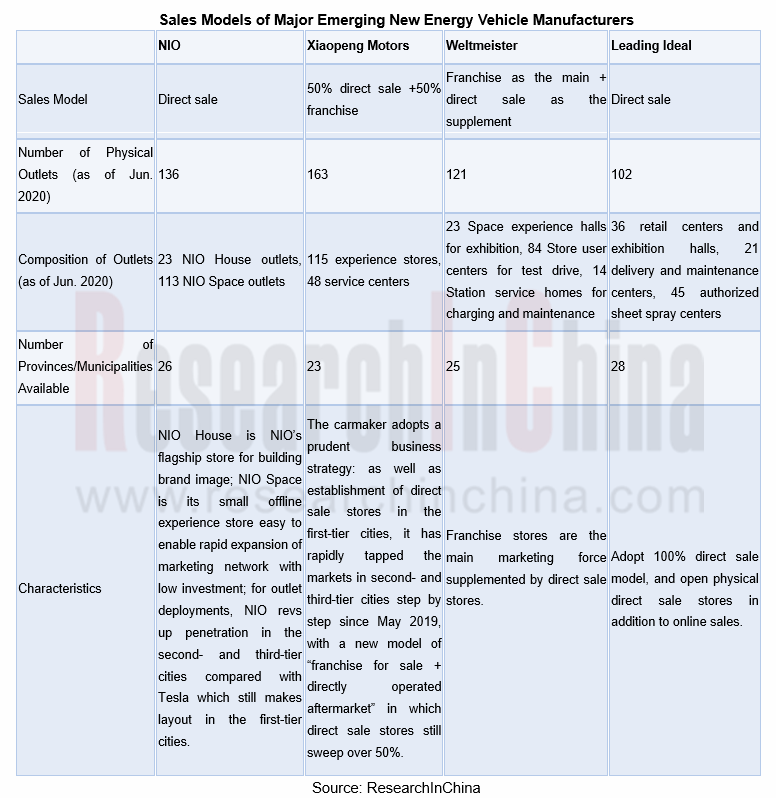

Emerging automakers adopt branding sales models and channels differing from the nationwide dealership model of conventional auto brands, changing from dealership model to direct operation of chain stores by auto brands or their cooperation with authorized dealers. The direct sale model offers totally different brand experience by providing full life cycle services for users, which serves as a solution to drawbacks of the common dealership model, such as non-transparent price and bad user service experience. Yet this model with some disadvantages like enormous investment and complicated operation process does not apply to all new energy vehicle manufacturers. 4S stores still need to shake up their service and profit structures even if they continue to employ the dealership model.

Automobile aftermarket refers to all the car-centric services needed by consumers in the period from post-sale to scrap. The growing aftermarket, especially maintenance and repair segment is accompanied by aging vehicles. That’s because the older the auto parts, the more frequent repairs they need and the more they cost. In current stage, the average vehicle in China is 5 years old, and those aged 4-10 seize over 58%. Vehicle aging, and increasing ownership are dual effective booster to prosperity of the aftermarket, making it a new industrial hotspot. The industry will usher in a boom period.

Automobile aftermarket involves maintenance and repair, auto finance, used car, rental, accessories, beauty and refit, recycling, and aftermarket alliance platform integration/car e-commerce, among which auto finance, maintenance & repair, and used car are the top three segments.

Used Cars

Factors such as household demand, profession, consumer preferences, etc. will prompt car owners to replace or resell their cars in the circulation market through used car dealers, used car e-commerce platforms and other channels. In recent years, the state and local governments will make more efforts to promote automobile consumption with favorable measures which will drive used car consumption and fuel Chinese used car market to grow with larger scale of transactions. In 2020, China saw approximately 14.34 million used cars transacted, with the estimated value of RMB888.8 billion. Although the annual transaction volume dropped by 3.9% in the entire 2020 due to the epidemic, the domestic used car transaction volume experienced consecutive growth from March to December. In the future, the used car market is expected to occupy more market share in the automotive aftermarket.

Repair and Maintenance

In the context of high ownership, aging of vehicles and changes in the maintenance concept, the auto repair and maintenance market continues to swell. The annual repair and maintenance cost increases year by year as vehicles become older, because the number of repairs and the expenses of each repair for old and worn auto parts jump each year. Learning from the experience of developed countries, China is about to see the demand for repair and maintenance hit the peak. In the past ten years, automobile sales volume has been impressive while the growth of new car sales volume has slowed down. In the future, the average vehicle age will continue to rise, which will boost the auto repair and maintenance industry into a golden age. The scale of China's auto repair and maintenance had reached approximately RMB1,332 billion as of 2019, and is expected to hit RMB2,458 billion by 2026, surpassing the auto finance market to rank first in the aftermarket. Amid the anti-monopoly, independent auto repairers are gradually eroding the market share of traditional 4S stores. With the help of the "Internet +" model, the independent repair model will develop more radically.

Auto Finance

Auto finance refers to a variety of financial products for companies, individuals, governments, automotive operators and other entities. It centers on automotive OEMs, stretching to the upstream and downstream of the industry, and eventually to end consumers. Typical auto finance products include dealer inventory financing, auto consumption loans, auto leasing and auto insurance. In recent years, the overall penetration rate of China's new car finance has ascended year by year, like 43% in 2019. According to the proportion of cars involved with financial products, the loan penetration rate is about 35% and the financial leasing penetration rate 8%, meaning loans still lead by a high margin. Compared with mature markets in Europe and America, China's auto finance market for new cars has enormous potentials. As terminal consumption upgrades and credit is widely accepted, auto finance will witness further growth. The car sales volume has fluctuated and the growth rate of the auto finance market has slowed down (about 20%) since 2017, but the momentum of auto finance is more robust than the trend of the car sales volume. In 2019, the overall scale of China's auto finance market reached approximately RMB1.58 trillion, of which licensed auto finance companies accounted for approximately 50%.

China Automotive Distribution and Aftermarket Industry Report, 2020-2026 sheds light on the followings:

Introduction to the automotive distribution industry and aftermarket, including definition, classification, industrial chain, business models, etc.;

Introduction to the automotive distribution industry and aftermarket, including definition, classification, industrial chain, business models, etc.;

Global and Chinese automotive distribution market scale and forecast, including total automobile sales volume, dealer networks, dealers’ automobile sales volume, competitive landscape, new energy vehicle sales models, etc.;

Automotive aftermarket segments, including market size and forecast, competitive landscape, industry trends, etc. of auto finance, used cars, repair & maintenance, beauty, etc.;

Profile, business analysis, brand agency, business networks and marketing of major auto dealers in China.

Global and China Leading Tier1 Suppliers’ Intelligent Cockpit Business Research Report, 2022 (II)

Tier1 Intelligent Cockpit Research: The mass production of innovative cockpits gathers pace, and penetration of new technologies is on a rapid riseGlobal OEMs and Tier 1 suppliers are racing for the i...

Global and China Leading Tier1 Suppliers’ Intelligent Cockpit Business Research Report, 2022 (I)

Tier1 Intelligent Cockpit Research: The mass production of innovative cockpits gathers pace, and penetration of new technologies is on a rapid riseGlobal OEMs and Tier 1 suppliers are racing for the i...

China Commercial Vehicle Intelligent Cockpit Industry Report 2021

Research on Intelligent Cockpits of Commercial Vehicles: Heading for Large Screens, Voice Interaction, Entertainment and Life

Following AD/ADAS functions, the intelligent configuration of the cockpit...

Automotive Ultra Wide Band (UWB) Industry Report, 2022

UWB got initially utilized in the military field, and began to be commercially applied after the release of criteria for UWB commercialization in 2002. In 2019, Car Connectivity Consortium (CCC) liste...

China Automotive Distribution and Aftermarket Industry Report, 2022-2027

Since the introduction of 4S store model into China at the end of 20th century, China's authorized dealer system has gradually developed from a single-store-based mode to a group-based mode, and from ...

Global and China Skateboard Chassis Industry Report, 2021-2022

Research into skateboard chassis: where to sell, how to sell and to whom it is sold

Rivian, a new carmaker based on skateboard chassis, is quite popular in the market and becomes the focus of the aut...

Emerging Automakers Strategy Research Report, 2022--NIO

Research on emerging carmaking strategies: no new cars in 2021, 3 new cars in 2022, can NIO make its renaissance?

The delivery of ET7 is imminent, and the sluggish sales situation is expected to fade...

Automotive and 5G Industry Integration Development Report, 2022

Research on integration of vehicle and 5G: OEMs rush into mass production of 5G models whose sales may reach 3.68 million units in 2025

By the end of 2021, China had built and opened in excess of 1.3...

China Automotive Finance Industry Report, 2022-2030

Auto finance is lucrative with the highest profit margin in the international automobile industry chain, contributing to roughly 23% of the global automobile industry profits. Yet, auto finance only h...

Global and China Power Battery Management System (BMS) Industry Report, 2022-2026

1. Robust demand from new energy vehicle spurs BMS market to boom

New energy vehicle sales have been growing rapidly worldwide over the recent years, reaching 6.5 million units with a year-on-year up...

ADAS/AD Chip Industry Research Report, 2022

Autonomous driving chip research: In addition to computing power, core IP, software stacks, AI training platforms, etc. are becoming more and more importantL2.5 and L2.9 have achieved mass production ...

Automotive Sensor Chip Industry Research Report, 2022

Sensor Chip Research: Automotive Sensors Have Entered a Technology Iteration Cycle, and Opportunities for Localization of Chips Are Coming Automotive sensor chips can obtain external environment ...

Automotive Cloud Service Platform Industry Report, 2021-2022

Research on Automotive Cloud Services: Based on 5ABCD, cloud services run through the R&D, production, sale, management and services of automakersWith the development of intelligent connectivity, ...

Global and China Cobalt Industry Report, 2021-2026

As a very rare metal and an important strategic resource for a country, cobalt gets typically utilized in battery materials, super heat-resistant alloys, tool steels, cemented carbides, and magnetic m...

Automotive Event Data Recorder (EDR) Industry Report, 2022

An event data recorder (EDR), sometimes referred to informally as an automotive black box, is a device or a system installed in vehicle to monitor, collect and record technical vehicle data and occupa...

Commercial Vehicle ADAS Industry Report, 2021

ResearchInChina has published the "Commercial Vehicle ADAS Industry Report, 2021", focusing on policy climate, ADAS installations, suppliers, etc., and with a deep dive into the prospects of Chinese c...

Automotive High-precision Positioning Research Report, 2022

High-precision Positioning Research: from L2+ to L3, high-precision integrated navigation and positioning will become the standard

With the development and progress of the autonomous driving industry...

China Around View System (AVS) Suppliers and Technology Trends Report, 2021 –Joint Venture Automakers

Research into JV automakers’ around view system: large-scale implementation of AVP is round the corner, and AVS vendors are energetically pushing ahead with parking fusion solution.

During January to...