Autonomous heavy truck research: entering operation and pre-installed mass production stage, dimension reduction and cost decrease are the industry solution

ResearchInChina released "China Autonomous Heavy Truck Industry Report, 2022", which combs through and summarizes R&D testing, product implementation and commercial operation of autonomous heavy trucks of current domestic leading autonomous driving solution providers and heavy truck OEMs.

AD heavy truck solution providers successively enter the actual operation and pre-installed mass production stage

ResearchInChina also released a research report on autonomous heavy trucks in August 2021. At that time, most autonomous heavy truck-related companies were busy in pulling investment, looking for logistics and OEMs while promoting road testing and technology iterations. On the one hand, the solution needs huge funds to maintain technology R&D and expand scale of test vehicles; on the other hand, they also expect their own technology to be implemented in OEMs and logistics fleets, and to really run on the road through a scaled fleet. By August 2022, the solution providers and OEMs are more advanced in autonomous/ takeover-free testing and commercial operations, and the focus gradually shifts from R&D testing to actual operations and pre-installed mass production.

Autonomous/ takeover-free testing

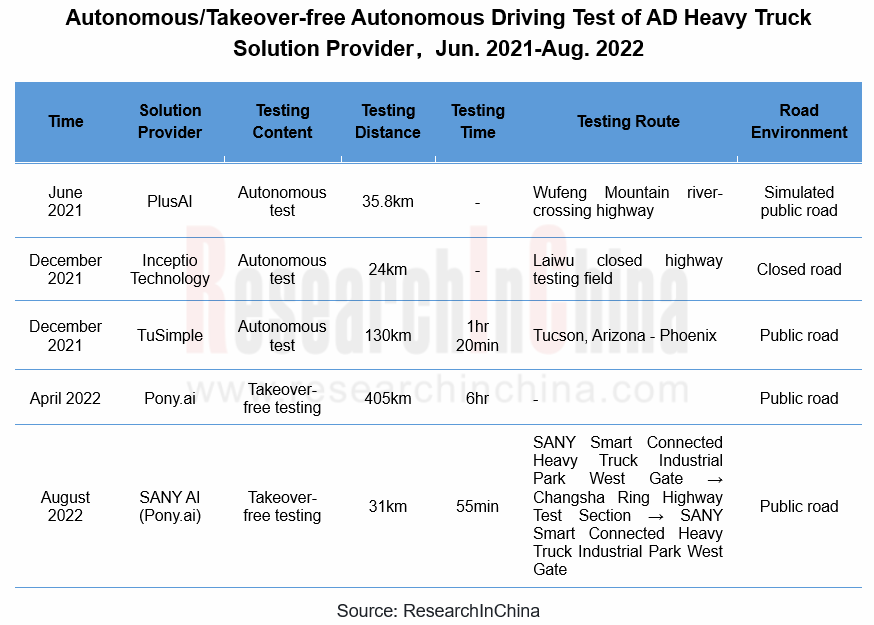

Starting in June 2021, the AD heavy truck solution providers gradually attempt to conduct autonomous or takeover-free public road testing for true real field autonomous/takeover-free technology validation. By August 2022, PlusAI, TuSimple, Pony.ai, etc. have all completed autonomous/takeover-free tests on public roads.

Among autonomous/takeover-free autonomous driving tests in the table above, TuSimple and Pony.ai are the most eye-catching.

According to the official statement, the fully autonomous test of TuSimple autonomous heavy truck on the public road took place at night, with no safety officers on duty or any human intervention throughout. The test was 80 miles long, including scenarios such as traffic signals, on and off ramps, emergency lane change vehicles and lane changes, and took 1 hour and 20 minutes. The entire test was conducted in close cooperation with Arizona Department of Transportation and law enforcement, with three safety and security vehicles in front of and behind the test vehicle to ensure safety of fully autonomous test operation.

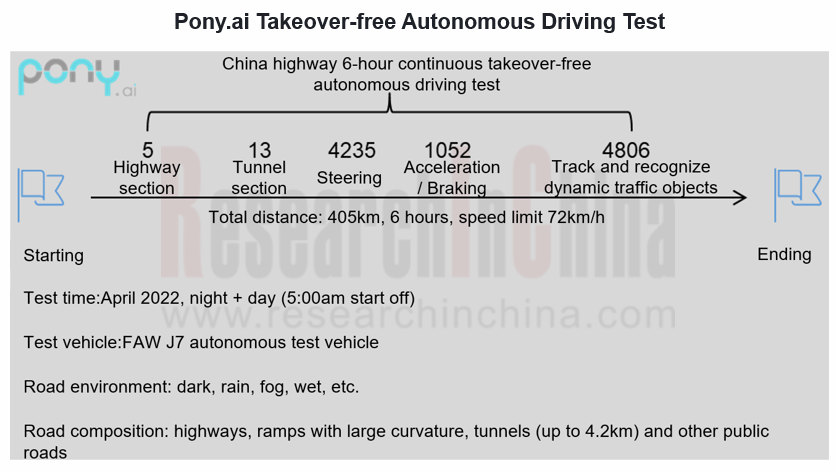

In April 2022, Pony.ai completed 6 hours of continuous, takeover-free autonomous driving tests in China's highway scenarios, going from night to day, through long tunnels, experiencing heavy rain and fog, and encountering real scenarios such as occupying accident cars, low-speed cars and special-shaped trailers. According to the official statement, in 6 hours, the driving distance exceeded 405 km, experienced 5 different highways and 13 tunnels, executed 4,235 turns, 1,052 accelerations/brakes, and tracked and recognized 4,806 dynamic traffic objects.

Commercial operations

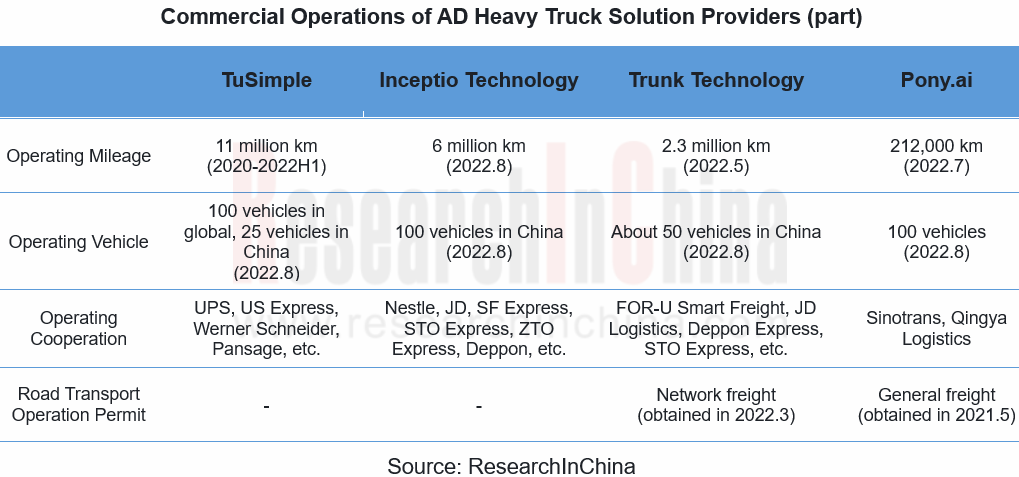

With the deepening of cooperation with logistics providers, solution providers have begun to show their strengths in actual road freight, allowing autonomous heavy trucks to earn freight. Trunk Technology and Pony.ai have obtained road transport operation permits and built their own fleets for transportation. Public data shows that the accumulated mileage of road transportation by TuSimple, Inceptio Technology, Trunk Technology and other solution providers have reached million-kilometer level, of which it has reached the most leading 7 million miles (about 11 million kilometers) during 2020-2022H1.

Pre-installed mass production

For capital, solution providers or logistics providers, what they are most looking forward to is the mass production and implementation of autonomous heavy trucks. Thus, the vehicle function, technical certification, vehicle sales and after-sales service and other related responsible parties can carry out road transport business activities.

The US RAND has estimated that an autonomous driving system needs to be validated for at least 11 billion miles (17-18 billion km) to reach mass production conditions. With a heavy truck driving 2000km in 24 hours, it would take 100 heavy trucks to drive about 240 years without stopping.

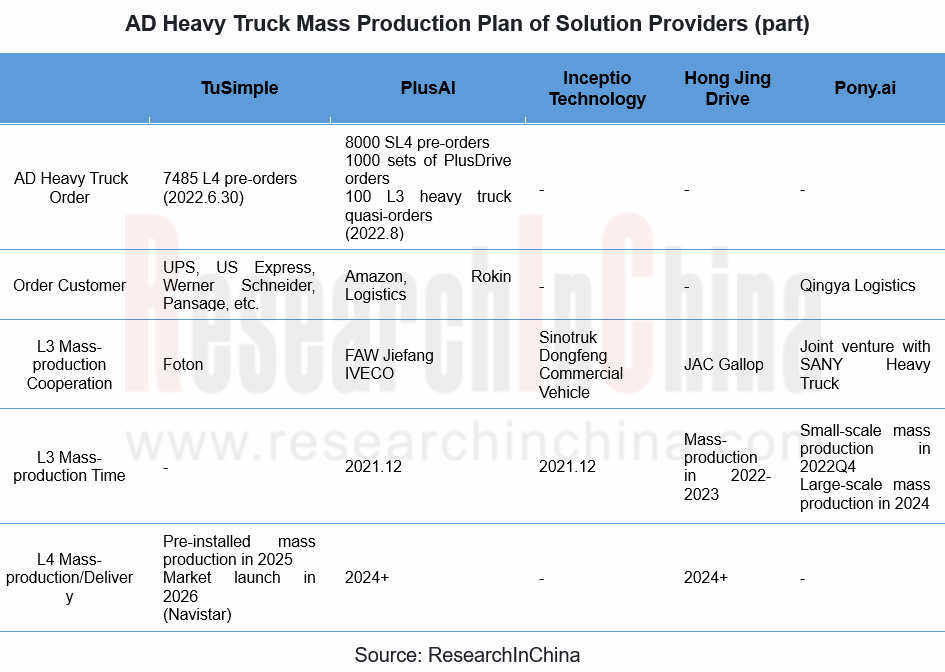

To obtain enormous real road test mileage, the only solution is pre-installed mass production and scaling to the market. At this stage, except for TuSimple, which insists on mass production of L4 heavy trucks, most solution providers are targeting L3 heavy trucks for mass production. They hoped that with mass production of L3 heavy trucks, autonomous driving system will run in large quantities on actual roads, thus obtaining massive road data, feeding back autonomous driving system and eventually realizing L4 autonomous driving.

PlusAI and Inceptio Technology, which are at the forefront of mass production, have each cooperated with heavy truck OEMs to produce L3 heavy trucks in late 2021 and have achieved some delivery results. In August 2022, PlusAI delivered five L3 FAW Jiefang J7 to its partner Rokin Logistics (with a total order of 100 vehicles, and the remaining 95 vehicles will be delivered within two years).

Big changes in autonomous heavy truck market

Emerging forces exist in passenger vehicle market, as well as in heavy truck market. Solution providers believe that the current traditional heavy truck manufacturers have many problems such as slow technical follow-up and unharmonious cooperation, which directly drag down the speed of mass production of autonomous heavy trucks. Therefore, in order to achieve better adaptation of software and hardware for autonomous driving and promote rapid implementation of autonomous heavy trucks, emerging forces such as DeepWay and Xingxing Technology have been established one after another. The biggest feature of heavy truck emerging forces is that they are built for autonomous driving, including fully redundant by-wire chassis, powertrain and cabin designed to meet needs of L4 autonomous driving.

Dynamics of some heavy truck emerging forces:

In September 2021, DeepWay released concept vehicle DeepWay-Xingtu, which is expected to be delivered in mass production in 2023.

In September 2021, DeepWay released concept vehicle DeepWay-Xingtu, which is expected to be delivered in mass production in 2023.

In April 2022, Xingxing Technology released Apebot I, an L4 autonomous pure electric van-type heavy truck for logistics, with mass production expected in 2023Q1.

In June 2022, Hydron, a hydrogen-fueled heavy truck company founded by TuSimple co-founder Chen Mo, is expected to deliver its first-generation products in 2024Q3.

Some time ago, Ministry of Transport released "Autonomous Vehicle Transport Safety Service Guide (trial)" (draft for comment), proposing that "under the premise of ensuring transport safety, encourage the use of autonomous vehicles to engage in road general cargo transportation business activities in scenarios such as point-to-point trunk road transportation and relatively closed roads." The document will provide greater space for autonomous heavy truck road transport services, facilitate technical verification testing of autonomous heavy trucks, and directly promote them from test vehicles to mass production vehicles.

Dimension reduction for L2+/L3 pre-installed mass production, becoming a practical choice for autonomous heavy truck solution providers

Solution providers all target long-term goal of L4/L5 autonomous driving, while most enterprises adopt a progressive development strategy, such as PlusAI, Inceptio Technology, Hong Jing Drive, etc. They reduce dimension of L4 solutions accumulated and verified over the years, enter the vehicle R&D and mass production process as Tier 1 or Tier 0.5, and enable heavy truck OEMs to jointly mass produce L2+/L3 models by packaging software and hardware solutions. For example:

Based on the R&D of L4 full-stack autonomous driving technology, PlusAI joined forces with FAW Jiefang to create a supervised autonomous driving heavy truck (L2 +/L3), and at the same time used the commercialization of mass-produced autonomous heavy trucks to carry out technical iterations.

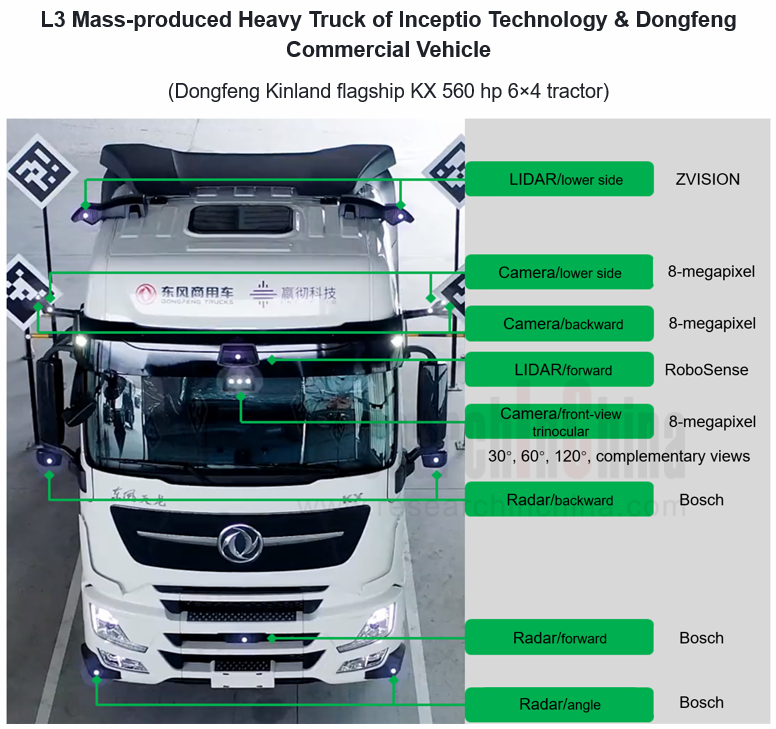

Inceptio Technology cooperated with Dongfeng Commercial Vehicles and Sinotruk to achieve mass production of L3 autonomous trucks, and a total of more than 200 vehicles of the two mass-produced models were rolled off the production line (as of August 2022).

For autonomous heavy truck solution providers, mass production is the most practical choice in the near future. On the one hand, reducing product purchase/modification costs can also obtain certain income; on the other hand, it can realize data closed loop through large-scale operation of mass production vehicles and drive technology iteration.

In-vehicle Communication and Network Interface Chip Industry Report, 2023

In-vehicle communication chip research: automotive Ethernet is evolving towards high bandwidth and multiple ports, and the related chip market is growing rapidly.

By communication connection form, au...

China Autonomous Driving Data Closed Loop Research Report, 2023

Data closed loop research: in the stage of Autonomous Driving 3.0, work hard on end-to-end development to control data.

At present, autonomous driving has entered the stage 3.0. Differing from the s...

ADAS and Autonomous Driving Tier 1 Research Report, 2023 - Foreign Companies

Research on foreign ADAS Tier 1 suppliers: 4D radar starts volume production, and CMS becomes a new battlefield.

1. Global Tier 1 suppliers boast complete ADAS/AD product matrix, and make continuous...

China Passenger Car Driving-parking Integrated Solution Industry Report, 2023

Research on driving-parking integration: with the declining share of the self-development model, suppliers' solutions blossom.

Local suppliers lead the driving-parking integration market.

The statis...

Passenger Car Cockpit Entertainment Research Report, 2023

Cockpit entertainment research: vehicle games will be the next hotspot.

The Passenger Car Cockpit Entertainment Research Report, 2023 released by ResearchInChina combs through the cockpit entertainme...

Smart Road - Roadside Perception Industry Report, 2023

Roadside perception research: evolution to integration, high performance and cost control.In June 2023, at a regular policy briefing of the State Council the Ministry of Industry and Information Techn...

China Passenger Car ADAS Domain Controller,Master Chip Market Data and Supplier Research Report, 2023Q1

Quarterly Report on ADAS Domain Controllers: L2+ and above ADAS Domain Controller Master Chip Market Structure This report highlights the passenger car L2+ and above (including L2+, ...

Automotive Cockpit Domain Controller Research Report, 2023

Research on cockpit domain controllers: various forms of products are mass-produced and mounted on vehicles, and product iteration speeds up.

Both quality and quantity have been improved, and the it...

Chinese Passenger Car OEMs’ Overseas Layout Research Report, 2023

OEMs’ overseas layout research: automobile exports are expected to hit 7.18 million units in 2025.

1. China’s automobile export market bucked the trend.

During 2021-2022, the global economy ...

Global and Chinese Automakers’ Modular Platform and Technology Planning Research Report, 2023

Research on modular platforms: explore intelligent evolution strategy of automakers after modular platforms become widespread.

By analyzing the planning of international automakers, Chinese conventi...

China Passenger Car Mobile Phone Wireless Charging Research Report, 2023

Automotive Wireless Charging Research: high-power charging solutions will lead the trend, with the installations to hit more than 10 million units in 2026.

Technology Trend: Qi2 Standard

The automo...

NXP’s Intelligence Business Analysis Report, 2022-2023

In 2015, NXP acquired Freescale for USD11.8 billion, hereby becoming the largest automotive semiconductor vendor. Yet NXP's development progress has not always gone smoothly. In 2021, Infineon replace...

Bosch’s Intelligent Cockpit Business Analysis Report, 2022-2023

Despite the chip shortage and the sluggish economy, Bosch’s sales from all business divisions bucked the trend in 2022. Wherein, the Mobility Solutions, still the company’s biggest division, sold EUR5...

Analysis on Baidu’s Intelligent Driving Business, 2022-2023

Baidu works on three autonomous driving development routes: Apollo Platform, Apollo Go (autonomous driving mobility service platform) and intelligent driving solutions. &n...

Ambarella’s Intelligent Driving Business Analysis Report, 2022-2023

Ambarella was founded in 2004 and is headquartered in California, the US. Before 2014, Ambarella was the exclusive chip supplier of GoPro. Ambarella was listed on NASDAQ in 2012. When the sports camer...

Global and China Electronic Rearview Mirror Industry Report, 2023

Electronic rearview mirror research: 2023 will be the first year of mass production as the policy takes effect

Global and China Electronic Rearview Mirror Industry Report, 2023 released by ResearchIn...

China Autonomous Driving Domain Controller Research Report, 2023

Autonomous driving domain controller research: explore computing power distribution and evolution strategies for driving-parking integrated domain controllers.

In China, at this stage the industry i...

China In-Vehicle Payment Market Research Report, 2023

China In-Vehicle Payment Market Research Report, 2023 released by ResearchInChina analyzes and researches the status quo of China's in-vehicle payment market, components of the industry chain, layout ...